Our regular round-up of Russian oil production, prices and Price Cap enforcement. I would also highlight coverage of our previous post in the Washington Examiner, Biden ignoring Pentagon, defense spending at pre-World War II levels.

Russian and Global Oil Markets

The EIA's monthly Short-Term Energy Outlook, issued this past Tuesday, reports Russian oil production rising to 10.76 mbpd in December, up a bit over the prior month. This is an impressive 200,000 bpd higher than the EIA expected just three months ago and the fourth consecutive monthly rise in Russian oil production.

The EIA has meanwhile updated its annual forecast for US oil production. In essence, this sees US production materially flat from September 2023 through the first half of 2025.

In fact, Russian oil production growth has marginally exceeded that of the US since August.

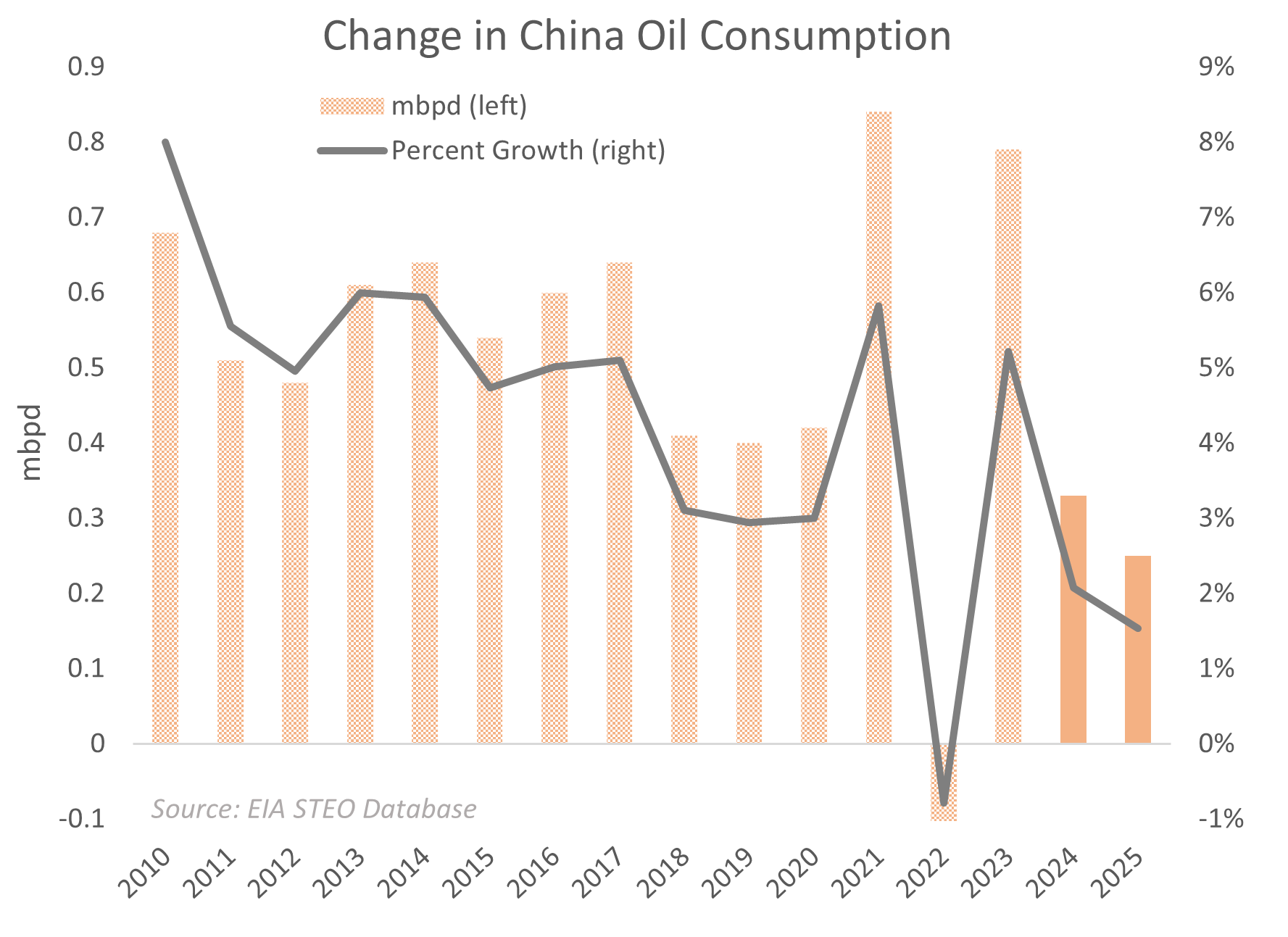

Flat US oil supply would ordinarily be bad news, as US shale oil production provided the discipline on oil prices for the last decade. However, two factors may mitigate the risk of an oil price surge. The first of these is weak anticipated demand growth from China. If all were well, we might expect annual oil demand growth of 3-5% or 0.5-0.7 million barrels per day / year (mbpd / year) in China. Nevertheless, the EIA anticipates growth of less than half this level, indeed, only 0.25 mbpd or 1.5% in 2025. This is consistent with the generally glum outlook for China.

Finally, OPEC is carrying surplus production capacity of approximately 2 mbpd over normal levels, and OPEC would ordinarily seek to deploy these reserves if the opportunity arose. Like weak Chinese demand, surplus capacity could act to suppress oil prices, which is good for Ukraine, as well as for the US and western Europe in aggregate.

Therefore, although plateauing US oil production would ordinarily be bullish for oil prices and negative for Ukraine, a poor outlook for China and ample OPEC production reserves suggest that oil prices could remain range-bound in 2024, and possibly beyond. On the whole, this appears positive for Ukraine.

Oil Prices

Brent closed on Friday at $78, largely in this range now for the last six weeks. A neutral price for Brent might be $82-87 / barrel, thus Brent would appear modestly below normal at present. Urals was similarly weak, closing Friday at $59, below the Cap limit for all of January to date.

Interestingly, the Urals discount, the difference between Russia's western oil export price and Brent, remains comparatively wide, averaging nearly $20 for the week. This is $6 greater than our forecast and suggestive of at least partial success in sanctions enforcement. Someone over at OFAC deserves a pat on the back for their sanctions work.

Ruble

The ruble appreciated marginally against the dollar this week, closing at 88 ruble / USD. This is largely unchanged in the last two months and contradicts recurring claims of a collapsing ruble.

Overall, oil prices remain favorable for Ukraine. We now need Congress to step up with some serious funding, notwithstanding fairly disastrous deficit numbers. Moreover, the Biden administration needs to refocus away from trying to seize Russian assets -- which are pretty well ring-fenced -- and instead restructure the Price Cap to capture the Urals discount and redirect this to Kyiv.