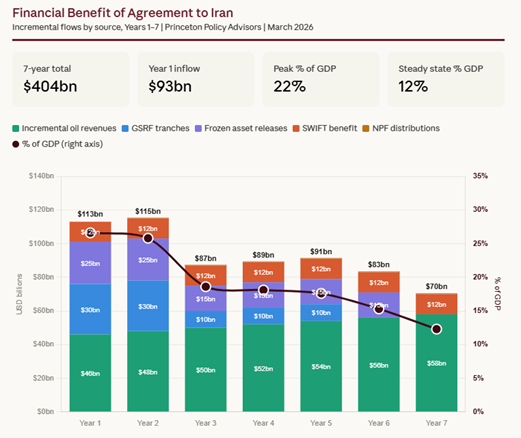

About $1 trillion, on a present value basis.

Iran is currently charging a toll of $1 / barrel or a maximum of $2 million per vessel to cross the Strait of Hormuz. At 20 mbpd of crude oil and refined products peacetime exports through the Strait, this amounts to, in round numbers, $40 million / day or $7.5 bn / year. All things considered, this would not meaningfully alter Iran’s financial situation or the fundamental nature of negotiations to end the war.

For purposes of an agreement with Iran, however, the underlying economic value of the toll should be the prime consideration. And this is very, very large.

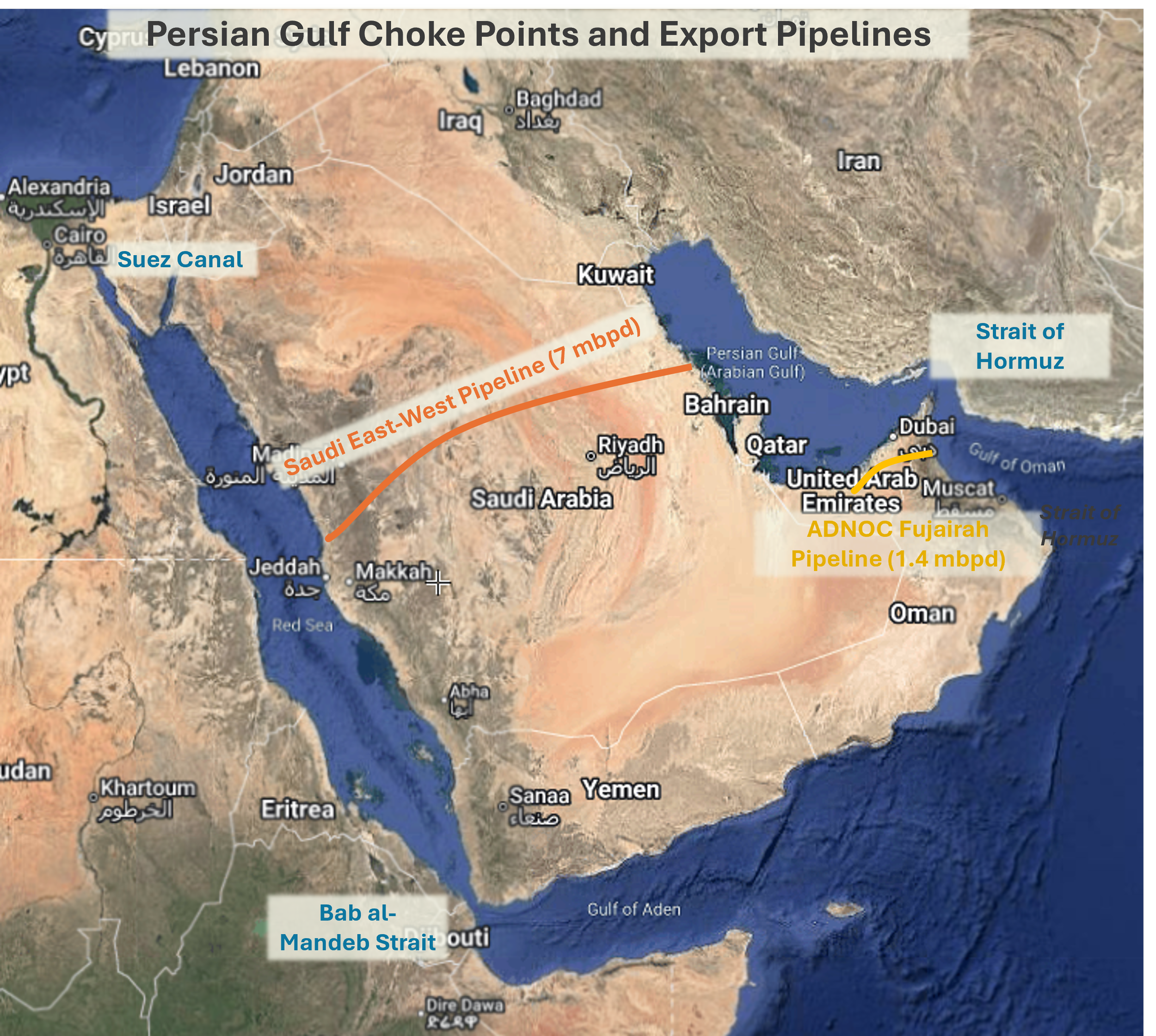

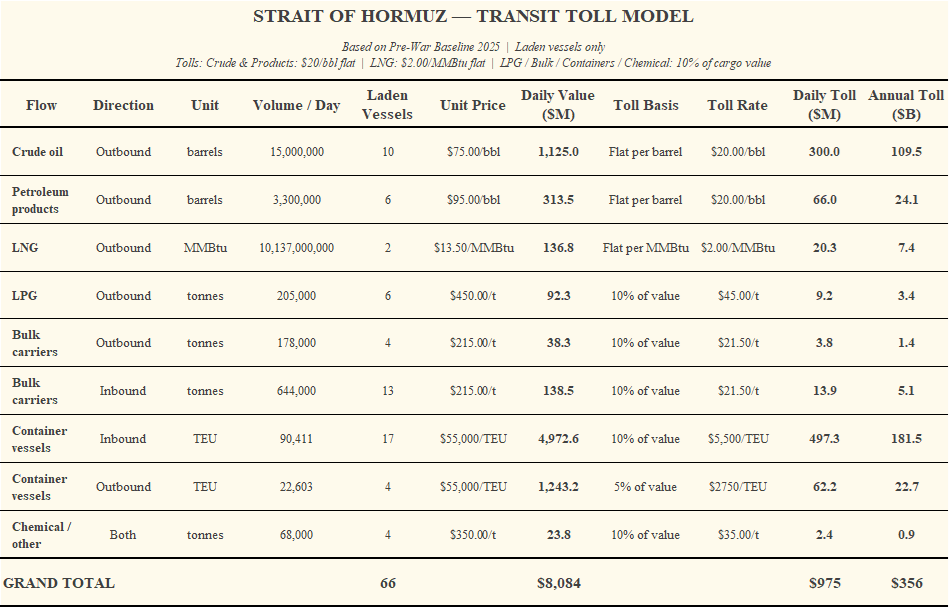

The media tends to focus on tankers, but in fact several types of vessels use the Strait, including crude and refined product tankers, container ships, bulk carriers and specialized vessels like LNG (liquefied natural gas) and LPG (liquefied petroleum gas) carriers. All of these are likely to be subject to tolls, sooner or later.

Nor should current Iranian pricing be deemed indicative of tolls after any agreement is signed. Monopoly service providers — and that is what Iran would be with respect to passage through the Strait — inevitably raise their rates to the level the market will bear. There are different ways to set prices, depending on how much political friction and alternative route development the Iranians are willing to tolerate. For now, I use unit toll values at the levels I would deem sustainable over the medium term.

The most visible and discussed item of trade in the Gulf is energy, notably crude oil, refined products like gasoline, as well as liquefied natural gas (LNG) and liquefied petroleum gas (LPG). Collectively, these represent $600 bn in annual exports from the Gulf.

This is, however, small change compared to the value of goods imported in containers. This is estimated at $1.8 trillion in imports and perhaps another $450 bn in exports, more than three times energy exports by value.

Bulk carriers and specialty tankers represent the balance, but these do not materially change the total of nearly $3 trillion in laden vessels entering and exiting the Strait annually.

Iran, if it is allowed control over the Strait, would be in a position to toll all of it.

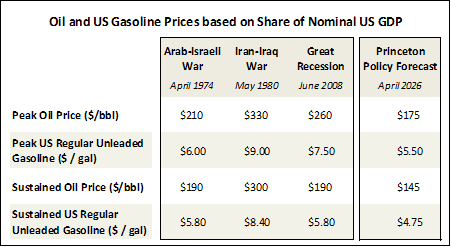

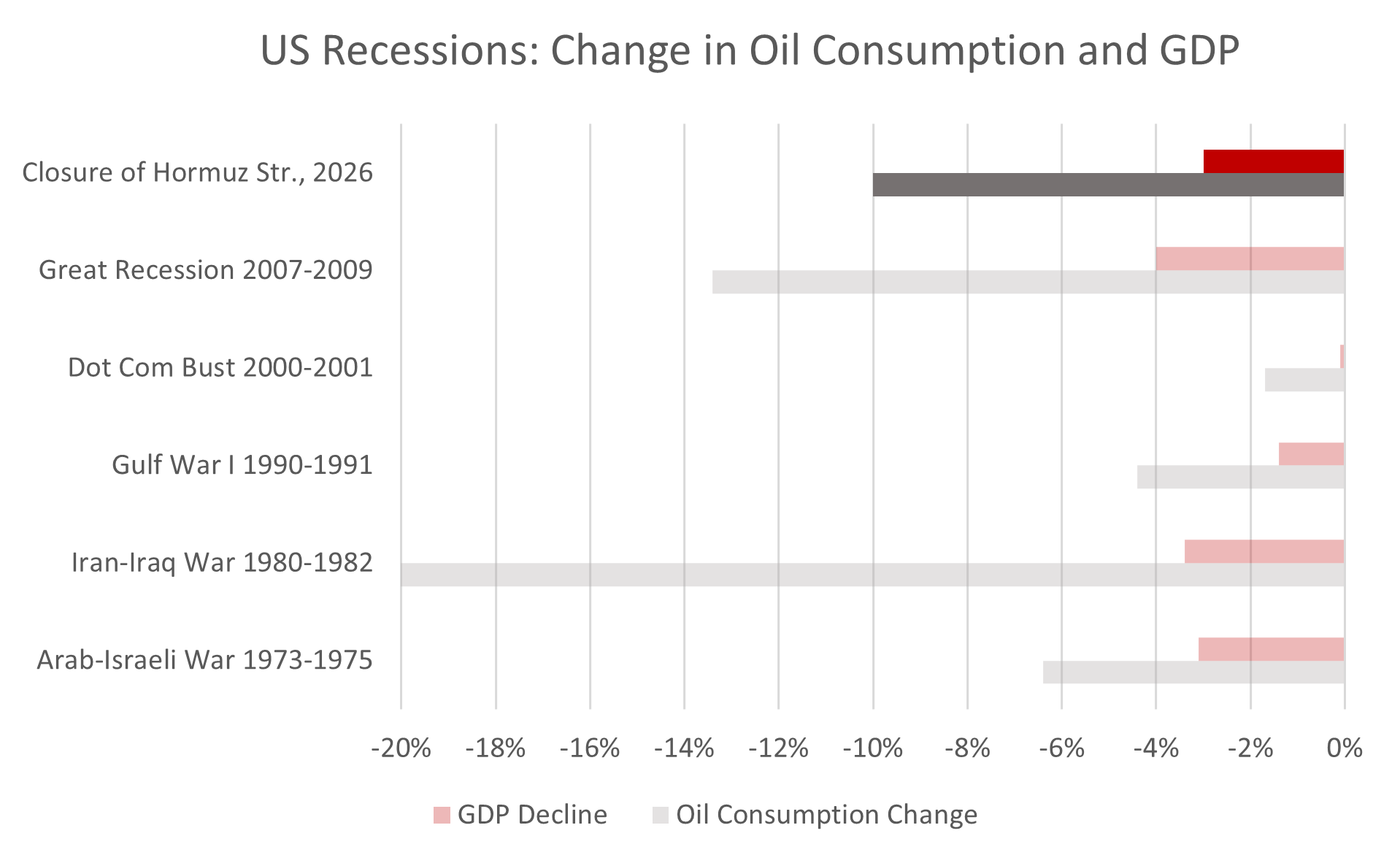

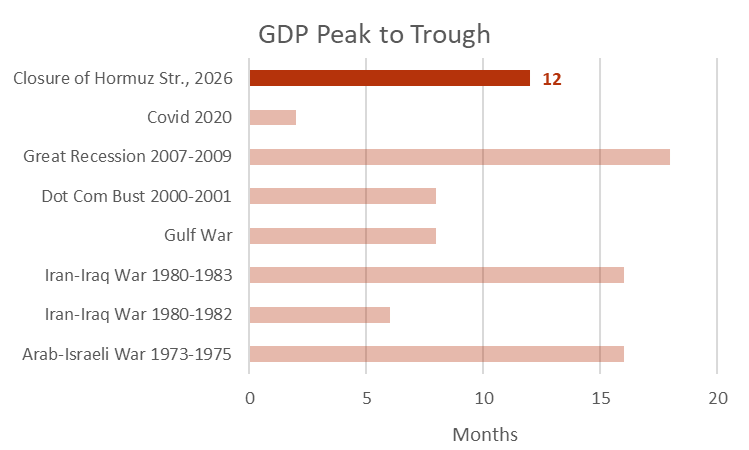

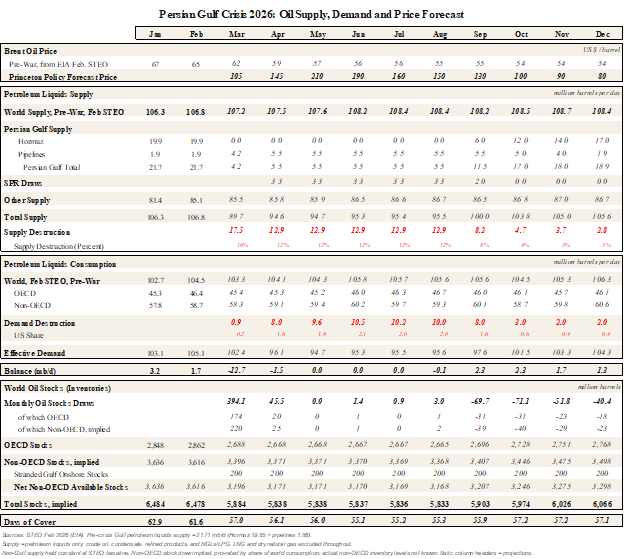

We estimate the sustainable toll on oil and product exports at approximately $20 / barrel, not the $1 / barrel currently charged. Even with such a toll, the oil exporters would still make hefty profits. Moreover, Iran and Russia collectively would control nearly two-thirds of global oil exports and materially all spare capacity under such a scenario and likely set oil prices higher than those observed before the war. As such, the Gulf exporters may not see a drastic reduction in net oil revenues, all things considered.

A $20 / barrel toll on energy exports would net Iran nearly $150 bn in toll revenues per year.

Container ships promises even greater returns. A 10% toll — a kind of tariff, to be more familiar to readers — would net Iran $200 bn in annual toll revenues.

In all, our estimates put Iran’s annual Hormuz toll revenues in excess of $350 bn.

Iran’s 2025 GDP in US dollar terms is estimated by various sources in the range of $350-420 bn. In other words, prospective toll revenues would reach 85% of Iran’s GDP. This sum would be transformative to the Iranian economy.

For negotiating purposes, one might value the toll at three times its annual value — a three-year payback period is a common ‘rule of thumb’ — which would imply an opening value for negotiating purposes around $1 trillion.

Of course, Iran will not see that amount. It does, however, set expectations for compensation for Iran. The hope that Iran will accept say, $20 bn or just the lifting of sanctions, is unlikely to be realized.

If the Trump administration is finding that its offers are being rejected one after another, it’s time to wake up and recognize underlying realities. A toll on the Strait of Hormuz has immense value to Iran. Any agreement to cede control over the Strait will have to provide commensurate compensation.

The US needs to make a better offer.