Russian Oil Production

The EIA published Russian oil production numbers for April, and for a change, they have come in at the EIA's expectations, that is, a decline of 350,000 bpd to 10.51 mbpd, down 7.3% compared to Russia's pre-war production.

Now, this would appear to be good news, but alas, not everyone believes it. Market Insider reports that, in the four-week stretch to May 5, Russia's "seaborne crude flows reached 3.55 million barrels a day, the highest mark since Bloomberg began tracking the data in early 2022. The rising seaborne exports continue a trend that was seen throughout March and April."

Given that Russia in February had ostensibly committed to reducing production by 500,000 bpd during March, resurgent exports have prompted skepticism from industry analysts. Russia has classified or delayed key statistics, including on oil production. Consequently, booming sea-borne exports of Russian oil and healthy refining volumes at home have prompted questions over whether Russia was indeed cutting its oil production. Under the circumstances, Russia's Deputy Energy Minister Pavel Sorokin felt compelled to hold a call with Western analysts, trying to convince them that Russia had reduced output as targeted. Reuters notes that the call was probably the first since early 2022. If Russians need to arrange a rare analyst call to convince the market that they are not cheating and lying, it is probably safe to assume that they are.

Nevertheless, according to Bloomberg, the number of idled oil wells in Russia rose to 18.1% of the total in March. Perhaps the Russians are cutting production after all, although the US could cut producing wells by 20% -- old stripper wells producing at most a few barrels per day -- without reducing output by more than a few percent. Time will tell.

Nearly all of Russia's crude exports were sent to China and India over the last month, and volumes to Asia also moved to a new high. China and India bought about 1.5 million barrels a day, according to Kpler data, and Turkey and Bulgaria were also top buyers.

So much for the embargo.

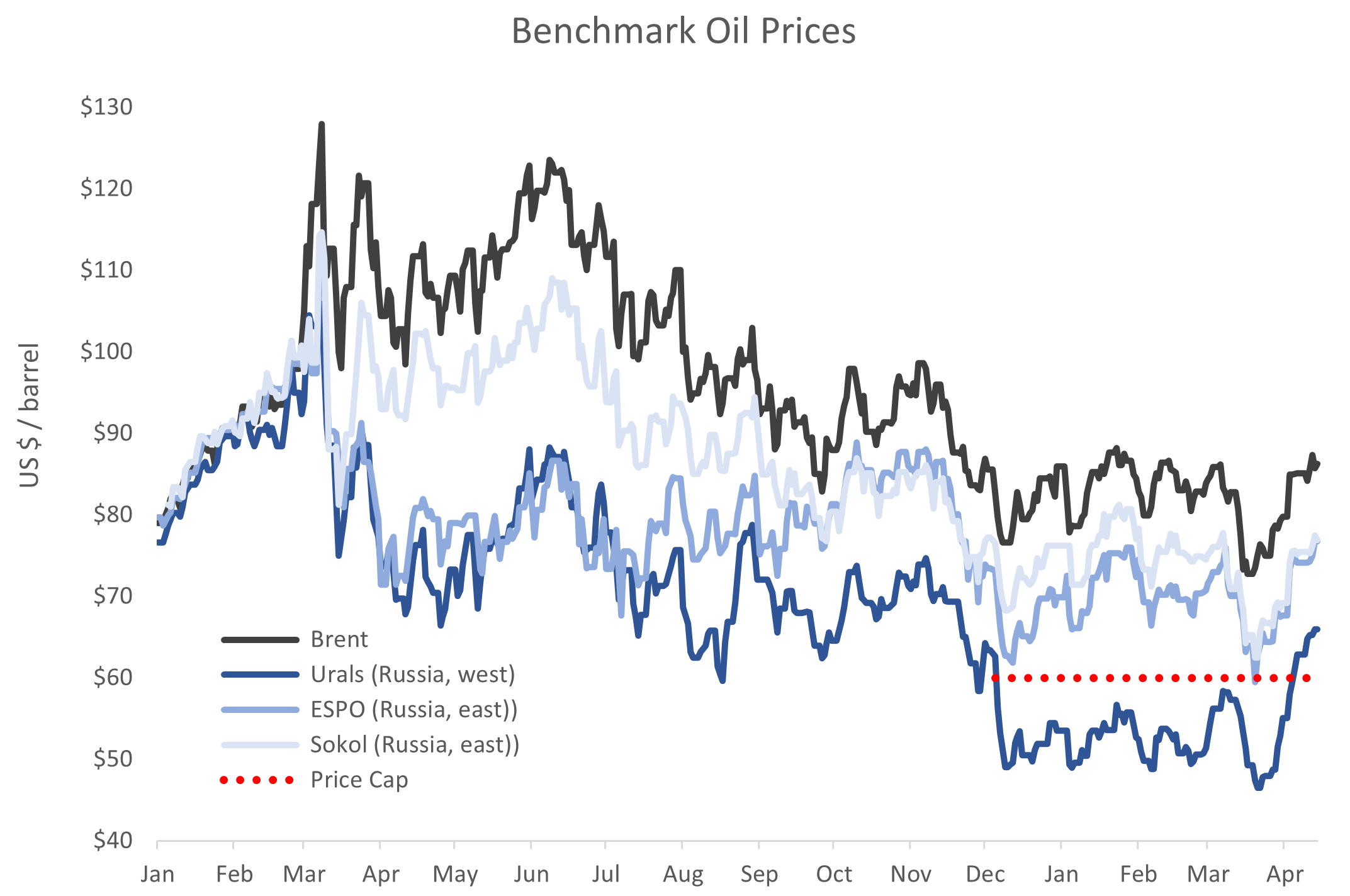

Oil Prices

Oil prices have languished in recent weeks, with Brent hovering in the mid-$70s. This in turn has translated into weaker Russian oil prices since mid-April, with Russia's benchmark Urals price returning below the $60 cap to around $56 / barrel.

Nevertheless, the Urals Discount -- the difference between the Urals and Brent oil prices -- remains smaller than before the implementation of the Price Cap or the Embargo. Perhaps the Discount will widen again, but it looks like the Russians have found a way around it. I would expect the Discount to shrink again, particularly if oil prices strengthen.

Overall, both oil pricing and trends in discounts were mildly unfavorable to Russia this week.

Russia's Budget

Oilprice.com notes that the Russian state is starting to accumulate financial reserves again. Speaking to Bloomberg, Natalia Milchakova, an analyst at Freedom Holding Corp., added that “this may even positively affect the ruble.”

Part of the reason for the recovery of oil revenues to the state budget is a tax hike. The government's take is based on an officially determined discount for Urals to Brent crude, which was set at $34 / barrel for last month. However, going forward, the base will be a narrowed discount to Brent, reaching $25 per barrel for July. According to the Russian Finance Ministry, the change in the formula could bring an additional $7.46 billion (600 billion rubles) into the federal budget. As a result, Moscow will likely begin buying foreign currency for its sovereign wealth fund again, with analysts expecting the purchases to begin in June and focus on the Chinese yuan.

In other words, continued elevated volumes of oil production, a trend towards a closing Urals discount, and a higher tax rate may allow Moscow to once again run a 'profit' on the war, in the sense of being able to accumulate, rather than draw, reserves.

So much for the Price Cap.

Conclusion

We have stated, for more than a year, that the Embargo and Price Cap would be failures, and the incoming data are consistent with our views. Given that former President Trump on CNN called for a reduced commitment to Ukraine were he to be re-elected, it is high time for the Ukrainians to take a more proactive role in the matter of Russia's oil export revenues.