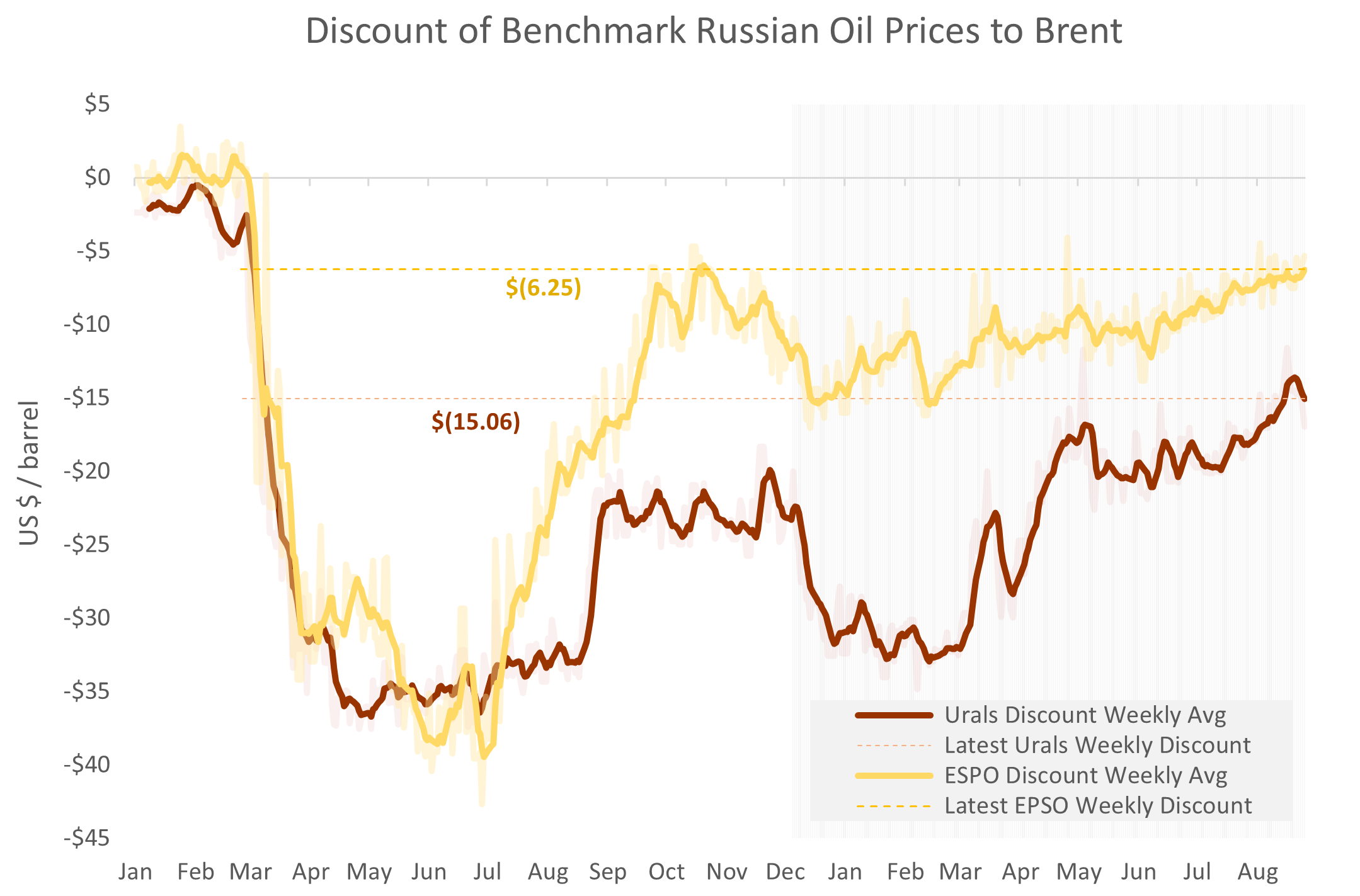

Urals, Russia's crude oil export price to the west, closed last week at $67.54, easing back on softer Brent pricing. Urals remain more than $7 / barrel above the Price Cap limit.

The Urals discount, the difference between the Urals and Brent oil prices, widened a bit to $15 / barrel for the week, but remains almost the smallest since the start of the war. The ESPO discount -- the difference between Russia’s Eastern Siberia - Pacific Ocean pipeline price and Brent -- continues to close and is on pace to disappear entirely by year end.

The takeaway remains as it was. The Price Cap is materially irrelevant. Urals is tracking Brent and the discount widens or narrows as Brent varies. When Brent is stronger, the discount shrinks. When Brent is softer, as it was this week, the discount widens.

As last week, the Urals price is close to its high since 2015 and is running at nearly $12 / barrel higher than its average for the 2015-2021 period. The Russians have reason to be pleased.

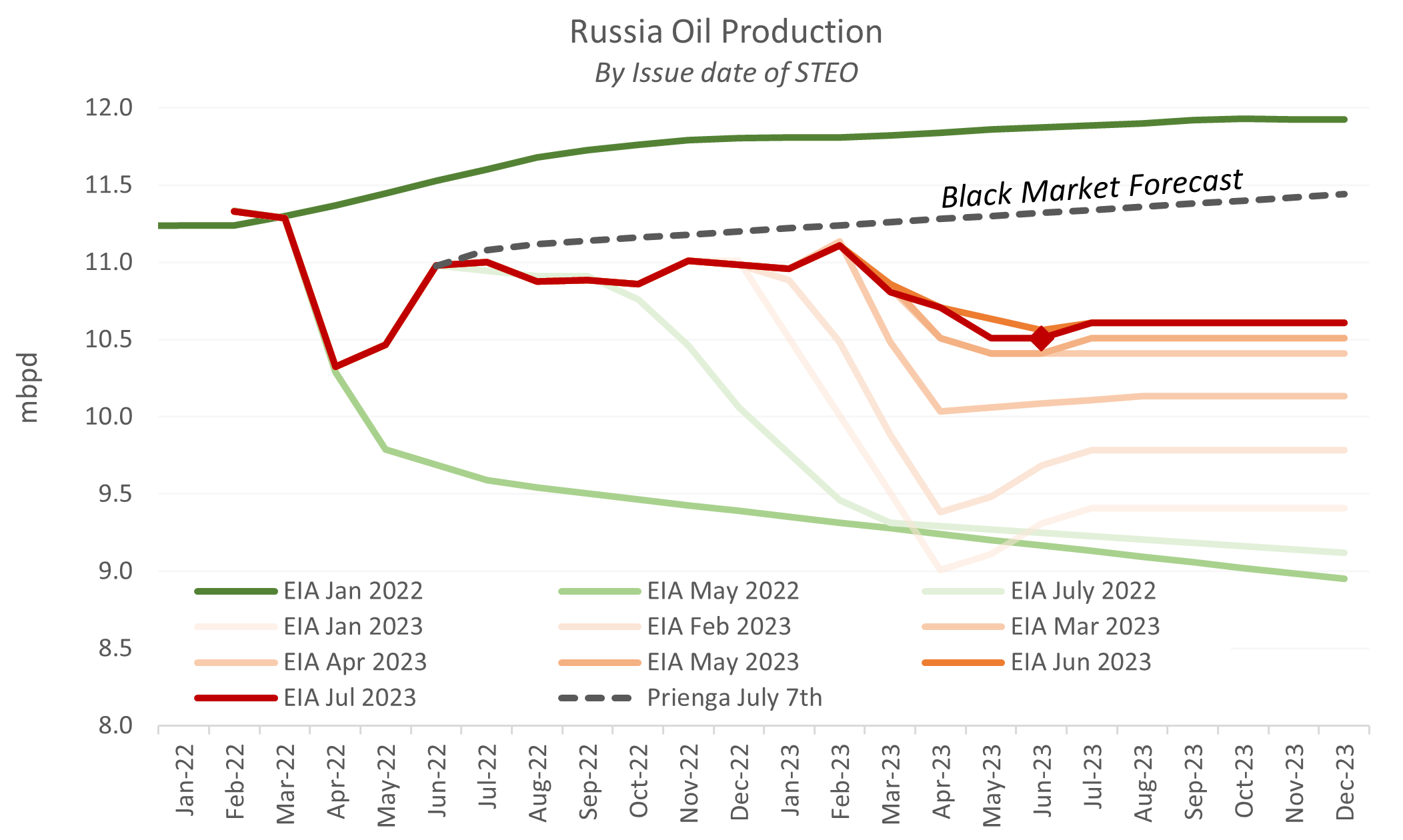

Indeed, Russia appears to be extending its production cuts and looks to cut exports by 300,000 bpd in September. The EIA estimated Russian oil production largely unchanged at 10.5 mbpd in July, which looks a pretty fair estimate given that the Russians have stopped reporting production levels in recent times.

Hysteria two weeks ago about a collapsing ruble has dissipated, and the ruble has stabilized under 95 / USD. This is not a surprise. Reported increases in the Russian money supply did not warrant an exchange rate beyond Rbl 100 / USD. Moreover, high oil prices and a collapsing Price Cap dictate improving Russian terms of trade, and that should underpin ruble strength. If one were to guess, go long the ruble here.

Overall, oil markets developments are favoring Russia at present. The Price Cap has visibly failed, OPEC+ production cuts are supporting oil prices, and the resulting terms of trade favor the ruble. As we are now in the last week of summer, on one cares in Washington DC, or to appearances, in Kyiv. Let's see if the mood changes after Labor Day. For Kyiv, the situation looks increasingly dicey. The Biden administration is more likely to paper over the failings of the current regime or admit defeat than to make necessary and constructive modifications to the Price Cap.