The press has generally reported that 20 mbpd, about 1/5th of global oil consumption, is at risk if the Strait of Hormuz in the Persian Gulf remains closed. The numbers are potentially larger. Further, don't expect either existing Middle East pipelines or releases from strategic petroleum reserves to materially change the picture.

Let's do the math.

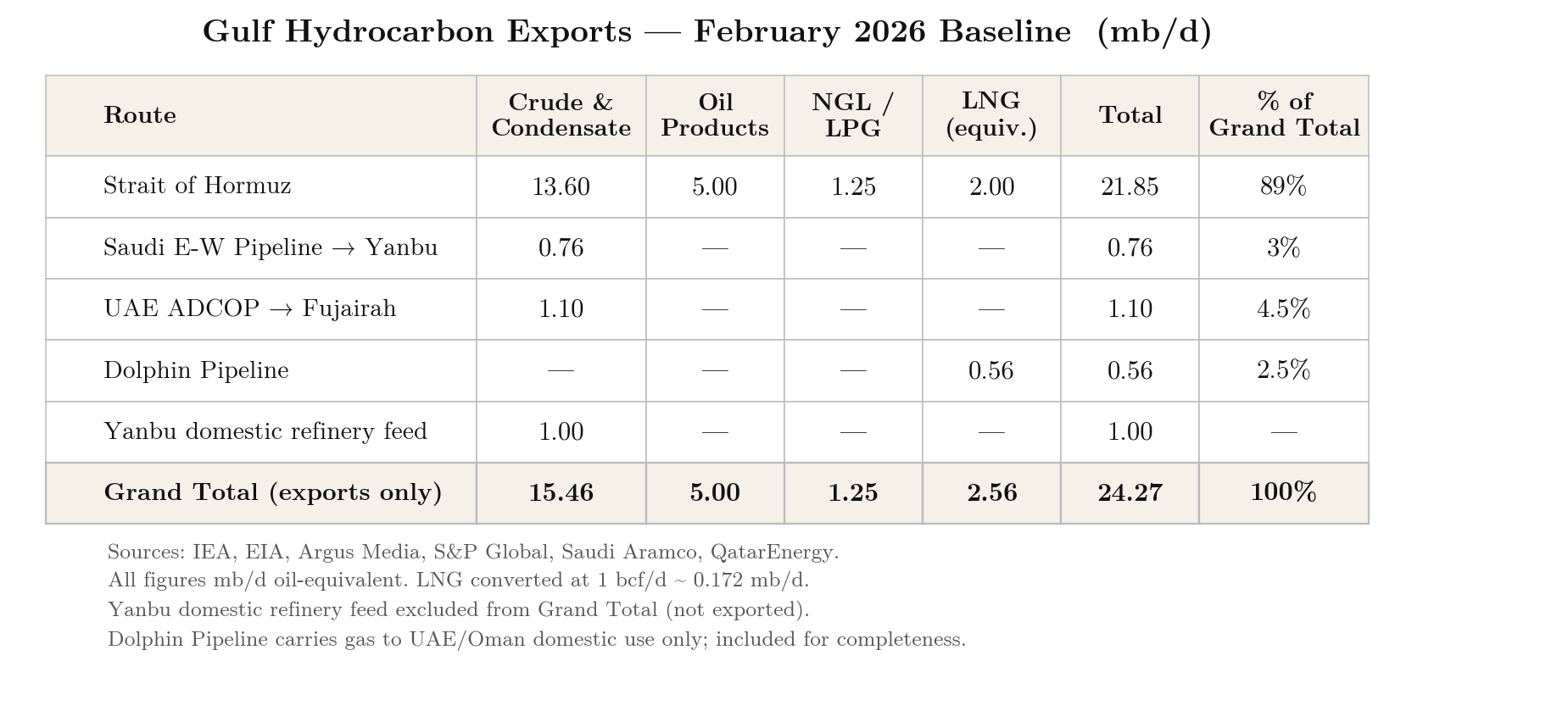

Tanker Trade: Pre-war, about 22 mbpd (million barrels per day) of petroleum liquids transited the Strait of Hormuz. Of this, about 14 mbpd was crude oil, and 5 mbpd was refined product like gasoline, diesel and jet fuel.

In addition, 1 mbpd was natural gas liquids (NGLs) like propane, butane and ethane transited the Gulf. NGLs are typically by-products of natural gas --not oil -- production and are rarely used for transportation.

Finally, the equivalent of 2 mbpd of liquefied natural gas (LNG) transited the Strait in February. LNG is natural gas which is cooled and compressed into a liquid state, allowing transport via specialized tankers. LNG is used principally for power generation, home heating and cooking, and various industrial applications. As with NGLs, LNG is not a transportation fuel.

Pipeline Transport: Before the war, about 3 mbpd of oil was also transported from the Persian Gulf via pipeline.

In total, about 25 mbpd of crude, products, NGLs and LNG were shipped from the Persian Gulf via tankers and pipelines immediately before the war.

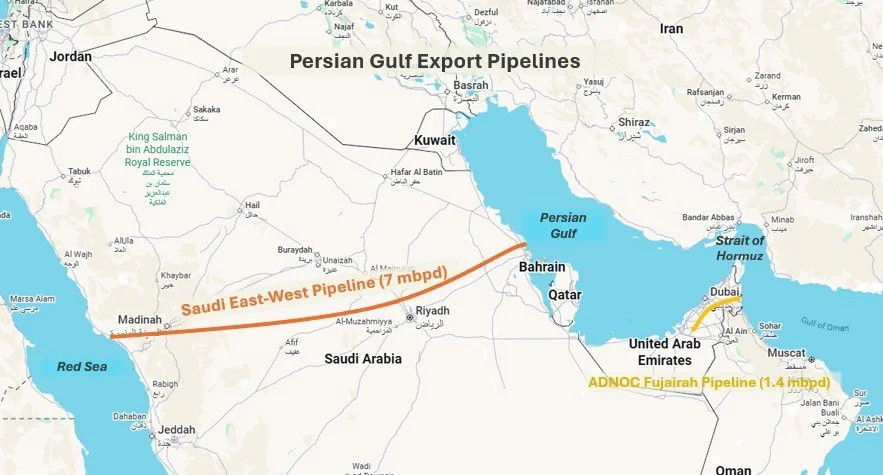

Diverting Hormuz Flows to Pipelines

How much could pipelines offset the closure of the Strait of Hormuz? The Saudi East-West Pipeline, with a capacity of 7 mbpd, runs to the port of Yanbu on the Red Sea. In February, the pipeline carried less than 1 mbpd and thus would seem to have 6 mbpd of spare capacity. However, Yanbu is thought to have loading capacity of only 4-4.5 mbpd; consequently, the pipeline's incremental export capacity probably does not exceed 4 mbpd.

The UAE also has an export pipeline to Fujairah, just beyond the Strait of Hormuz. This pipeline has a capacity of 1.4 mbpd, but was near full capacity in February.

All the export pipelines together probably represent no more than 4 mbpd of incremental capacity in practice, that is, they would offset no more than 1/5th of the losses from the Strait of Hormuz.

Spare Oil Production Capacity

To this we could add spare global oil production capacity of 4 mbpd. However, all of this is materially located in the Persian Gulf. As a result, there is no accessible spare capacity available.

Releases from Strategic Reserves

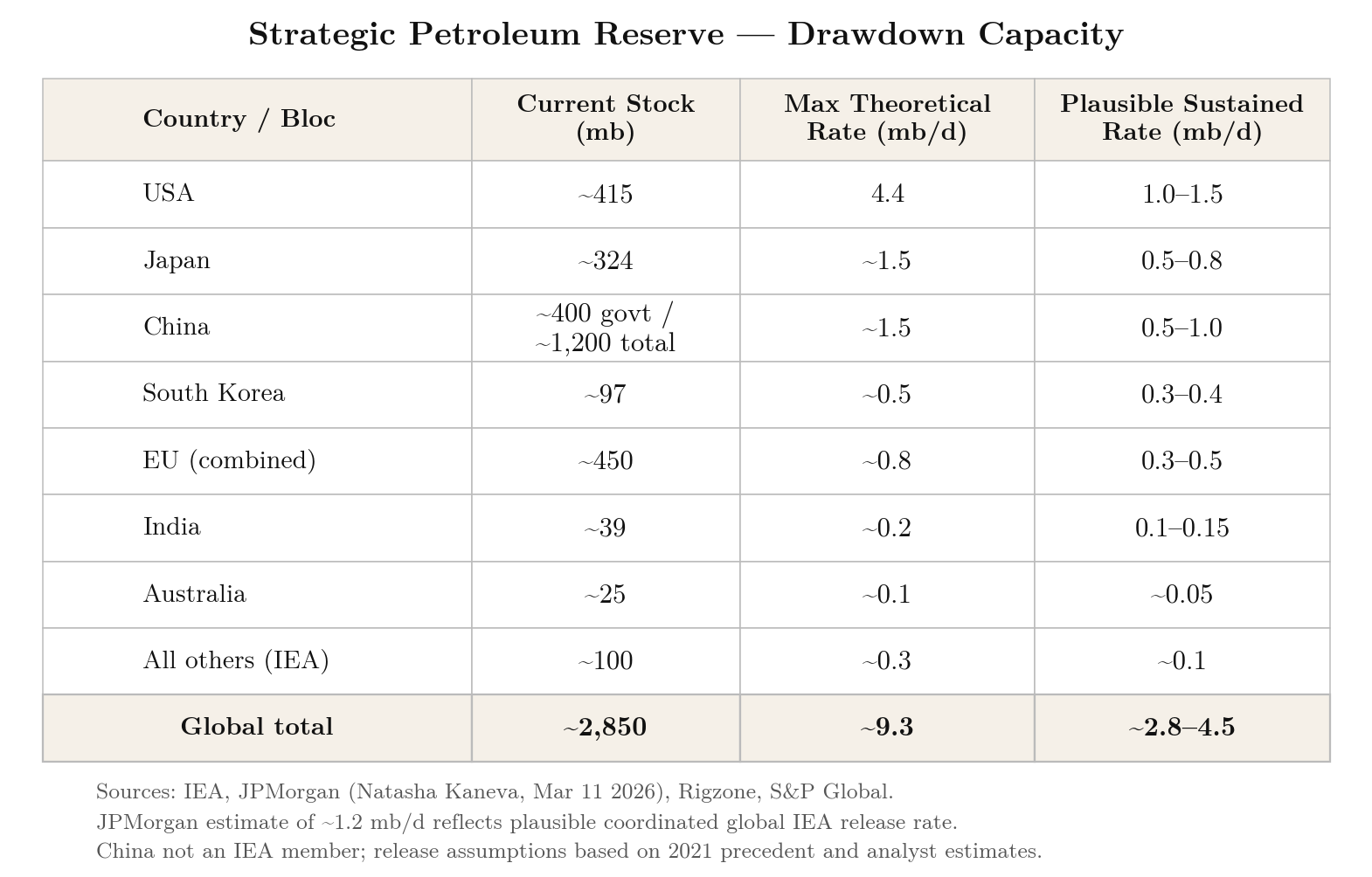

Finally, many countries have strategic petroleum reserves (SPRs). For example, the US SPR contains more than 400 million barrels of crude. Assuming all countries decided to deploy their reserves, the maximum theoretical SPR draw could reach 9 mbpd. The actual number is likely much lower. Most analysts surveyed by Rigzone projected SPRs to contribute 2-4 mbpd to supply, and even that with some delay.

The Bottom Line

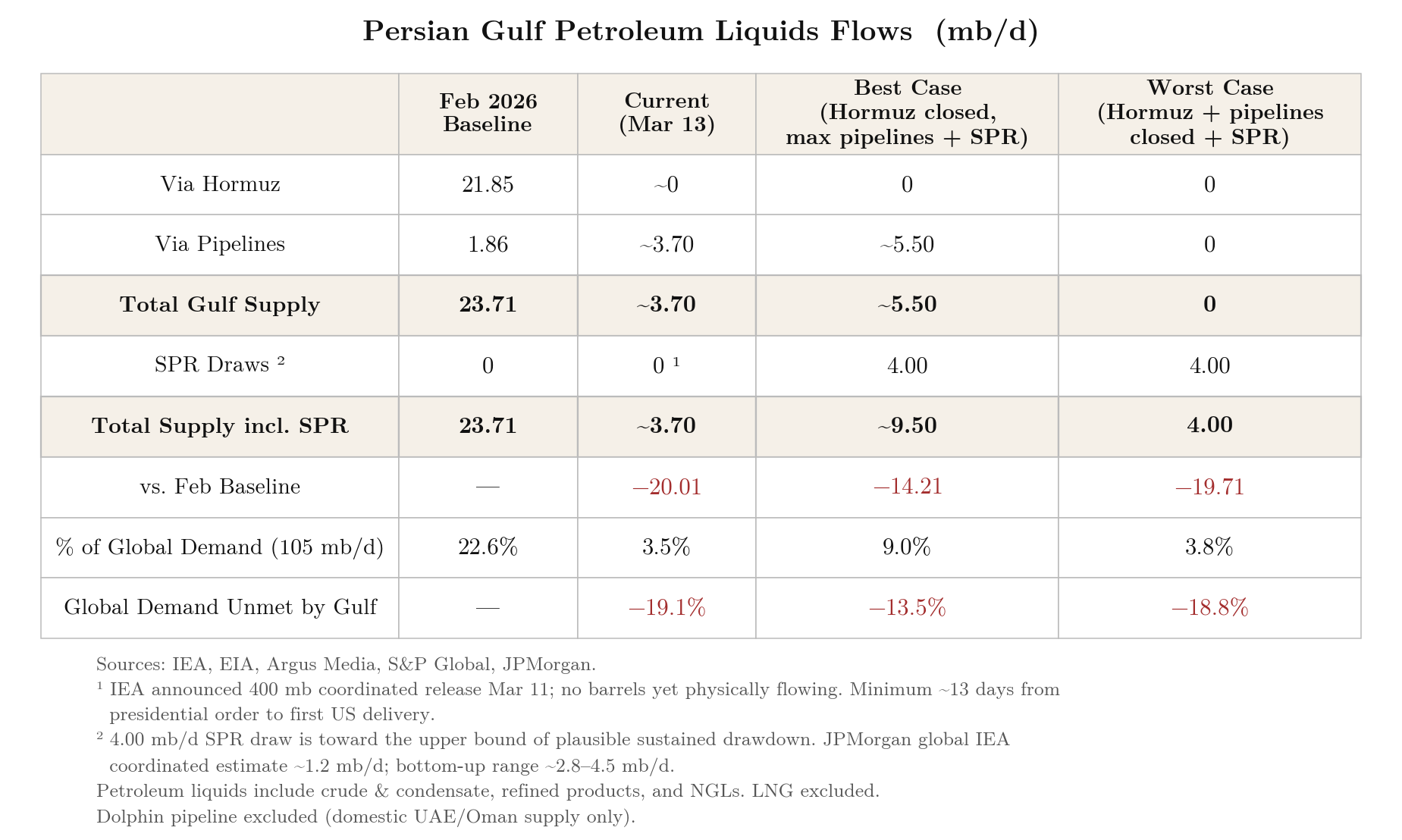

If the Strait remains closed, in the best case, oil exports could be redirected through spare pipeline capacity and supply could be augmented with SPR draws of 4 mbpd. Even in this scenario, however, global supply would still be down 14 mbpd, representing 14% of global consumption. By historical standards, this volume is three times that sufficient to induce an oil shock recession.

Finally, there is a worst case scenario in which Iran not only blocks the Strait, but also succeeds in disabling the region's vulnerable export pipelines. In such an event, even with SPR draws of 4 mbpd, global supply would lag demand by nearly 20 mbpd, or 19% of global oil consumption.

In summary, neither pipeline exports nor draws from strategic petroleum reserves will compensate for the closure of the Strait of Hormuz. Not even close. Indeed, the barrels at risk are greater than just those transiting the Strait. Iran may well be able to knock out the Saudi East-West and UAE Fujairah pipelines, raising the total outage to 25 mbpd, nearly a quarter of global oil consumption.

The Paris-based International Energy Agency (IEA) has described the closure of the Strait of Hormuz as the “largest disruption to crude supplies in the history of the global oil market." That is no exaggeration. If the US military is unable to clear the Strait within the next 30 days, expect a crushing oil shock recession.