Let's start with Price Cap metrics.

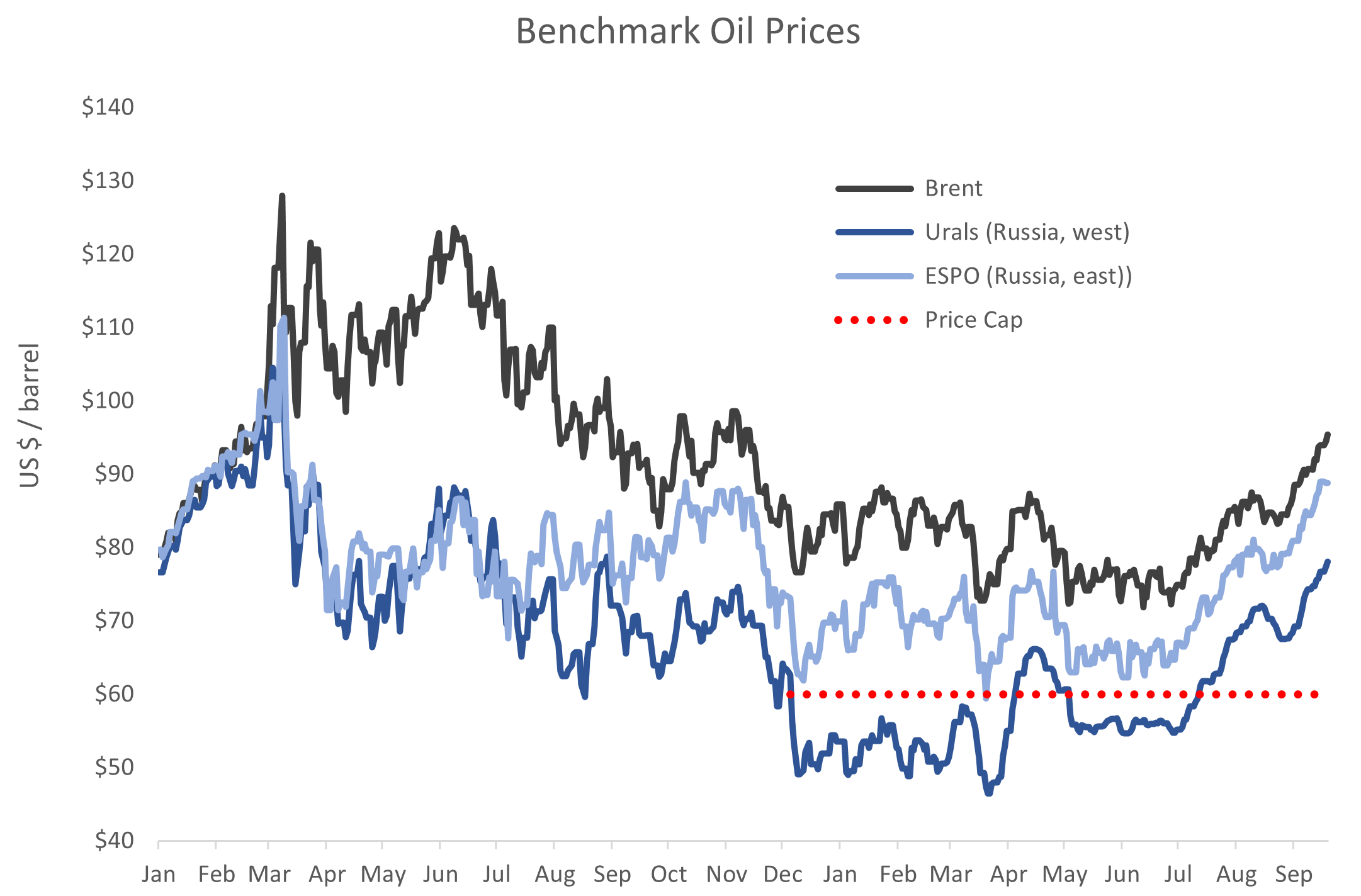

Brent and the Urals price had a ho-hum week, without material movement in either price. Brent closed the week at $85 / barrel, and Urals at $74. A wilting Brent is signaling weakness in the global economic outlook, but this happens from time to time without a broader downturn. But not always.

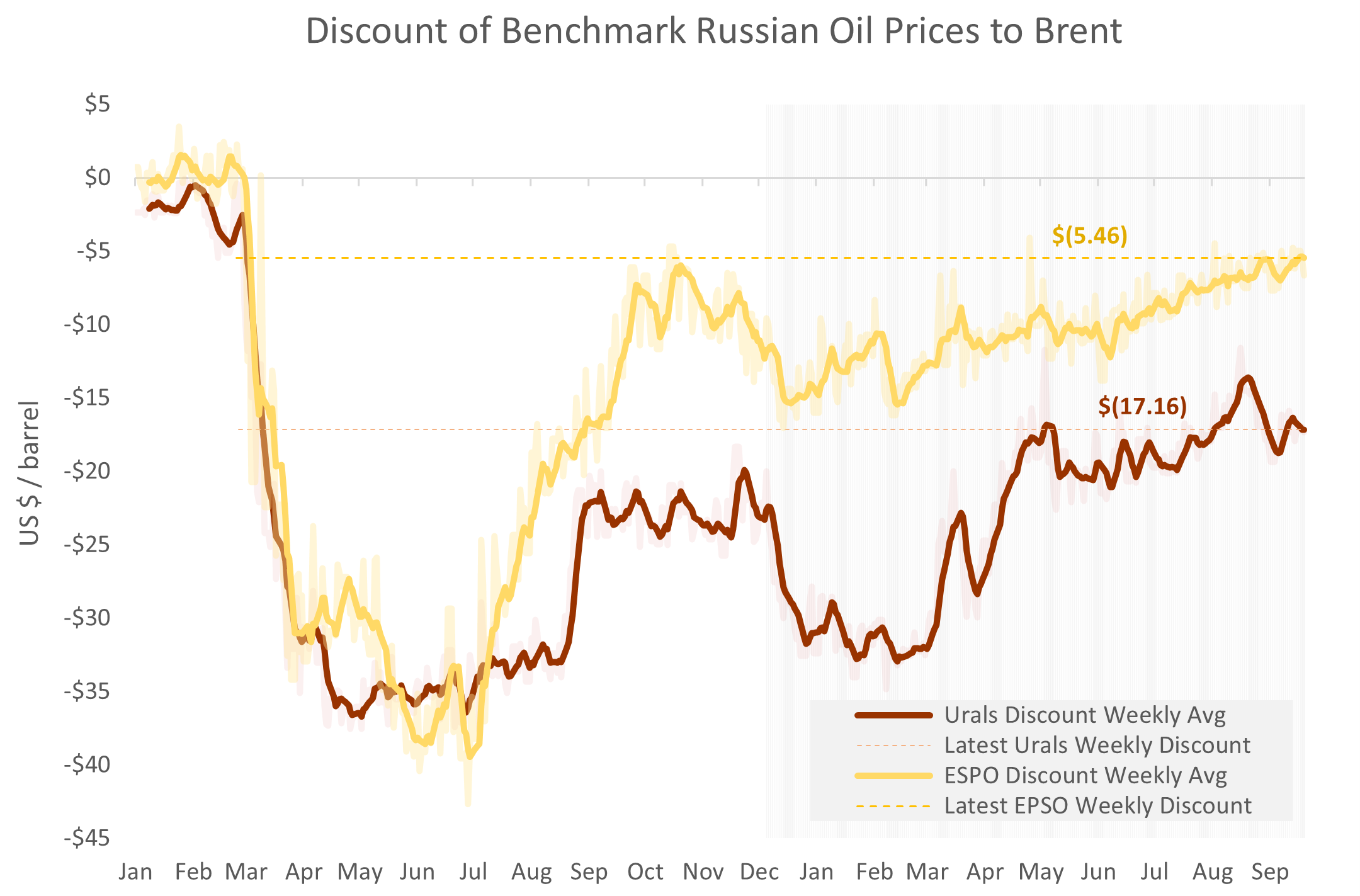

The Urals discount -- the difference between Russia's western crude oil export price and Brent -- continues to narrow, averaging $13.49 for the week and tightening by about $1 / barrel over the last month. Based on recent trends, expect the Urals discount to continue to decline by around $0.04 / day.

The ESPO discount -- the difference between Russia's eastern oil export price and Brent -- also continues to narrow, now under $5 / barrel. The ESPO discount may be expected to disappear entirely during the first quarter of next year.

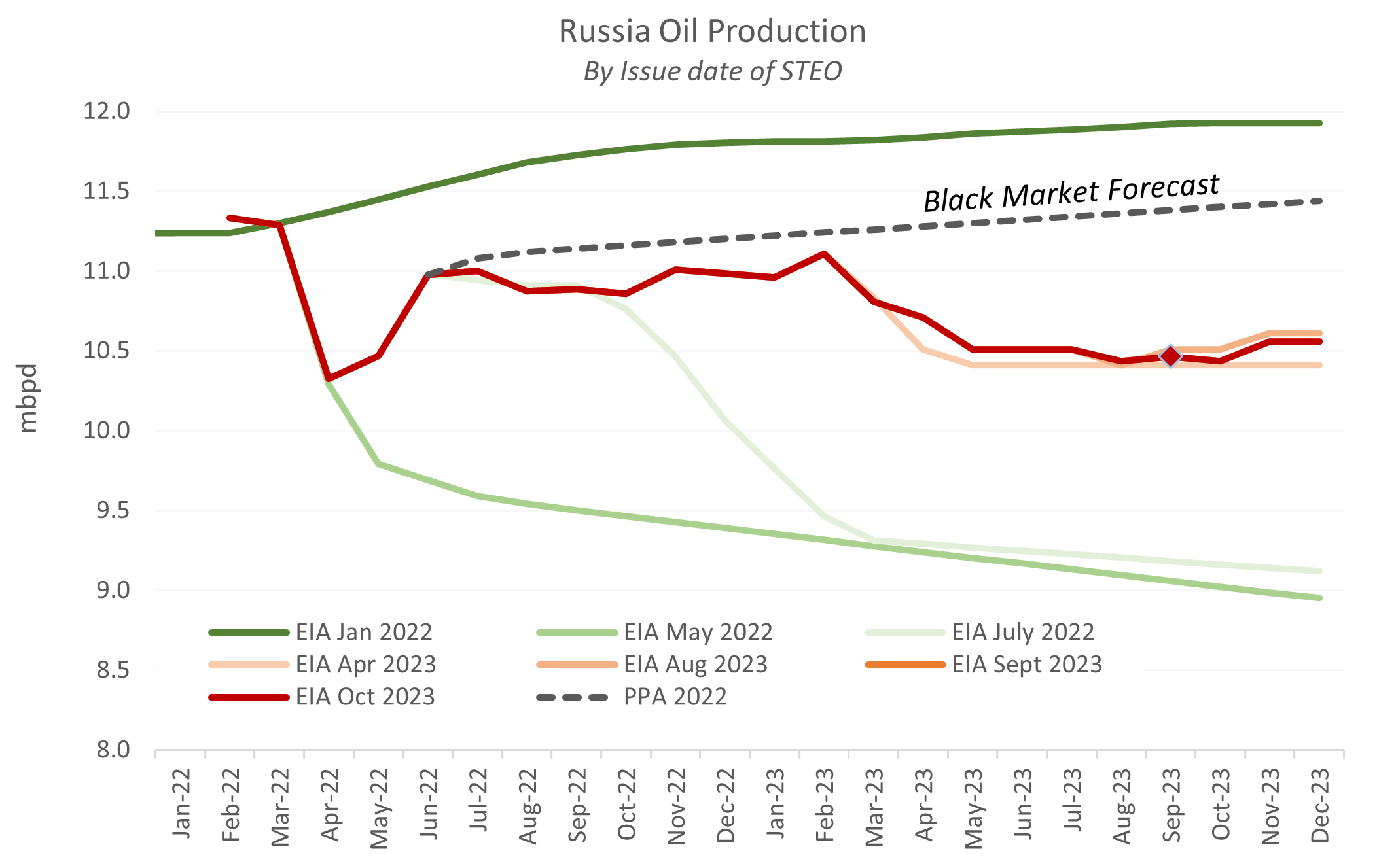

Bloomberg reports that Russia's seaborne crude exports averaged 3.7 mbpd last week, higher than the pre-war level and inconsistent with Russian promises to cut production. Nevertheless, according to Reuters, Russia's energy ministry said on Friday that crude oil and petroleum products exports collectively are slated to fall in November by more than 300,000 barrels per day (bpd), compared to the average level in May-June.

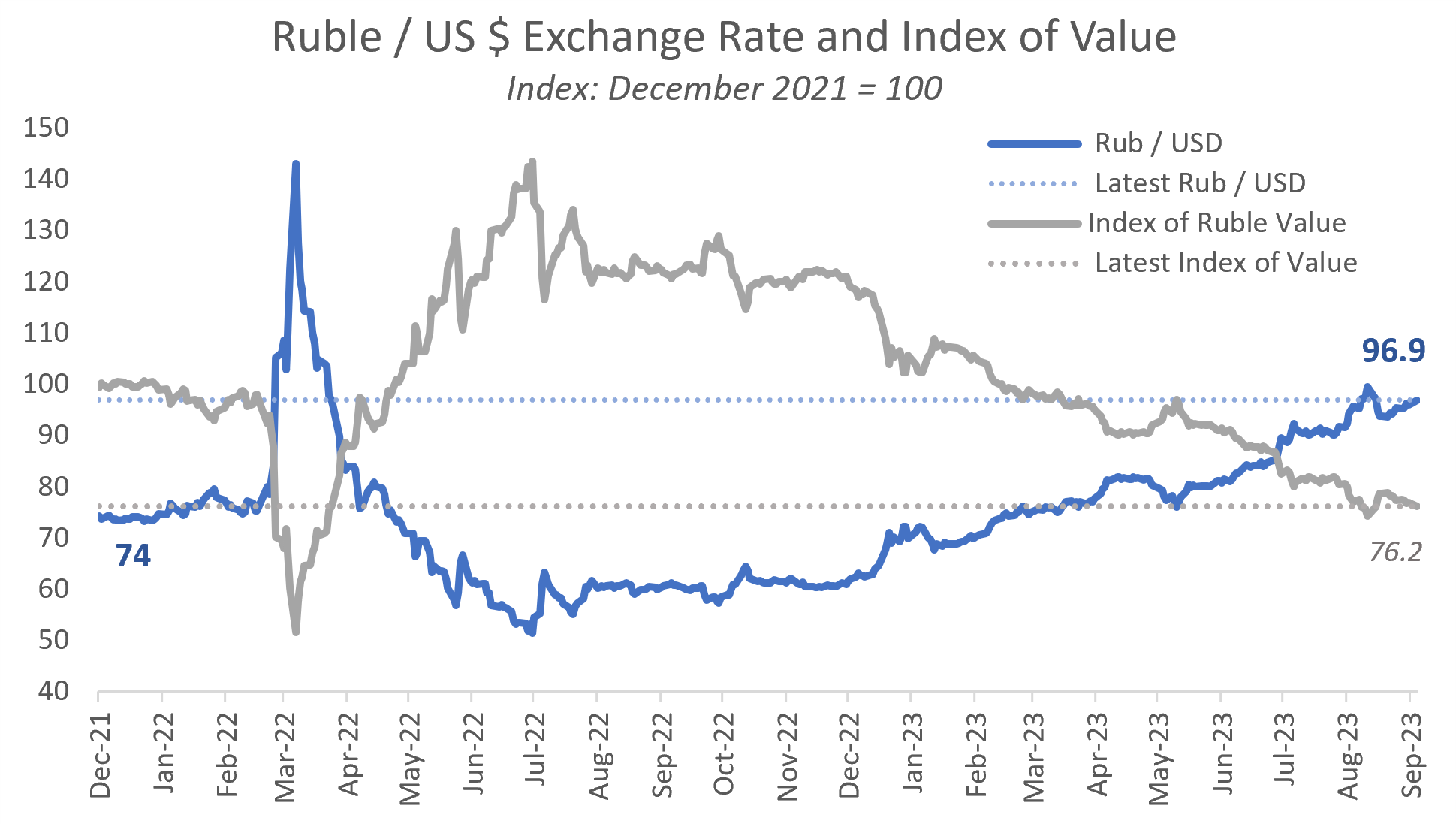

This past week, Russia's central bank hiked a key interest rate to 15%, up from 13%. The bank blamed higher-than-expected inflation. Readers will recall that I indicated increases in Russia's money supply were consistent with 20% inflation. Easy money appears to be propagating through the system, hence the rise in inflation. The Bank has stated that it is anticipating 7% inflation for 2023. This seems implausible. Russia's central bank probably uses some version of the Taylor Rule, which would imply inflation in the 12-14% range for a 15% interest rate. At a guess, Russia's true inflation rate is twice the figure claimed by the central bank.

Ordinarily, high inflation should lead to currency devaluation, but in fact, the ruble has appreciated by 8% on the US dollar in just the last few weeks. This is in part due to rising Russian interest rates, but also attributable to the collapse of the Price Cap and Russia's blended oil export price holding near $80 / barrel. Thus, Russia faces disparate trends, with elevated domestic inflation contrasting with substantially improving terms of trade internationally. I had stated earlier that I thought late summer hype about a collapsing ruble was likely overstated, and so it proved. Should Brent resume its rise, expect the ruble to appreciate further.

Finally, a newly released Gallup poll shows ebbing support for Ukraine in the US. A majority still supports Ukraine, but clearly, disappointment with a lack of material progress during the summer campaign has taken the wind out of the public's sails. Kyiv needs a rethink on financial and messaging strategy, and right now, the surreal passivity of the Ukrainian bureaucracy and Zelenskyy's inner circle is impeding action on these fronts.