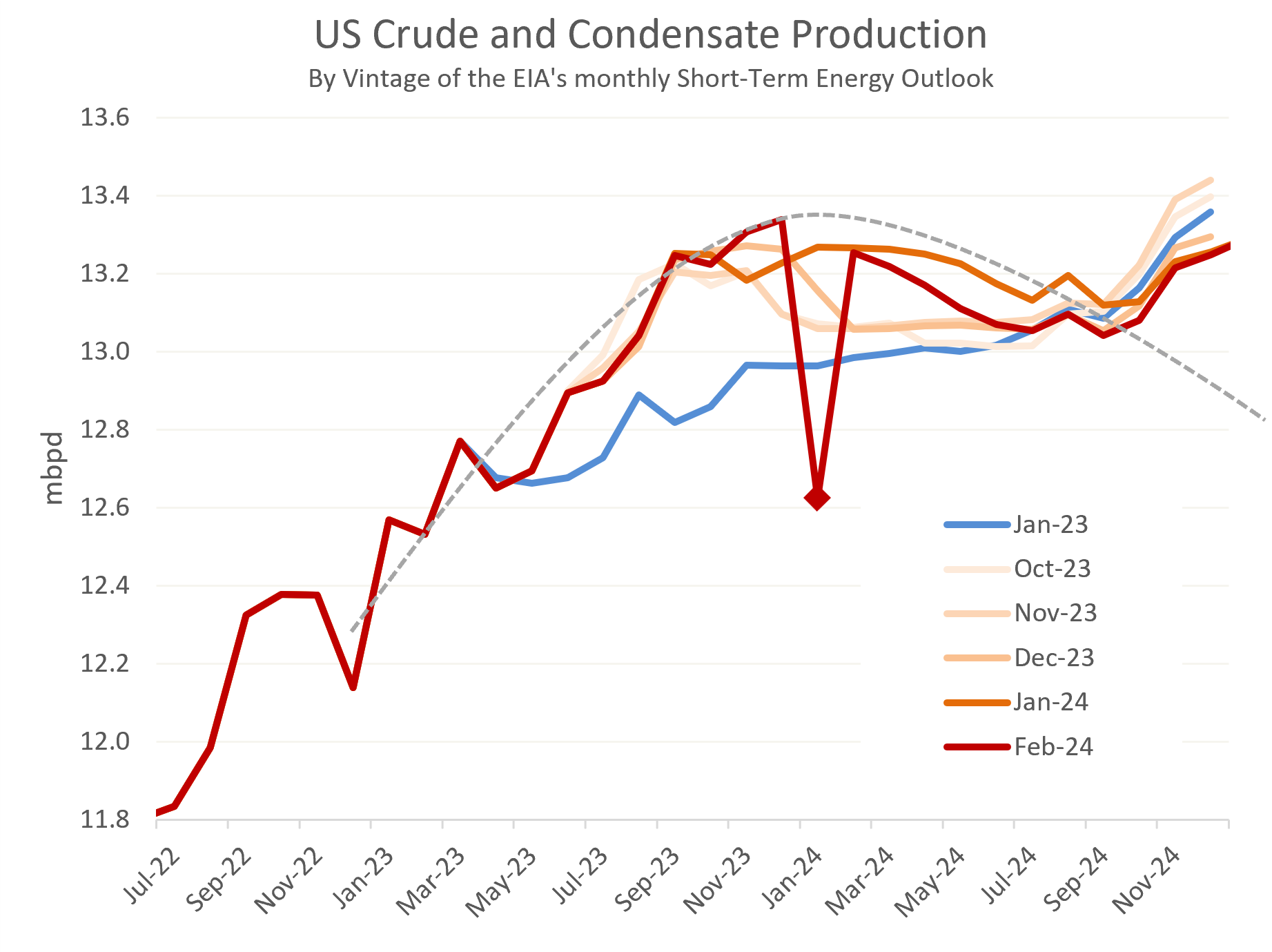

US Crude and Condensate Supply Outlook

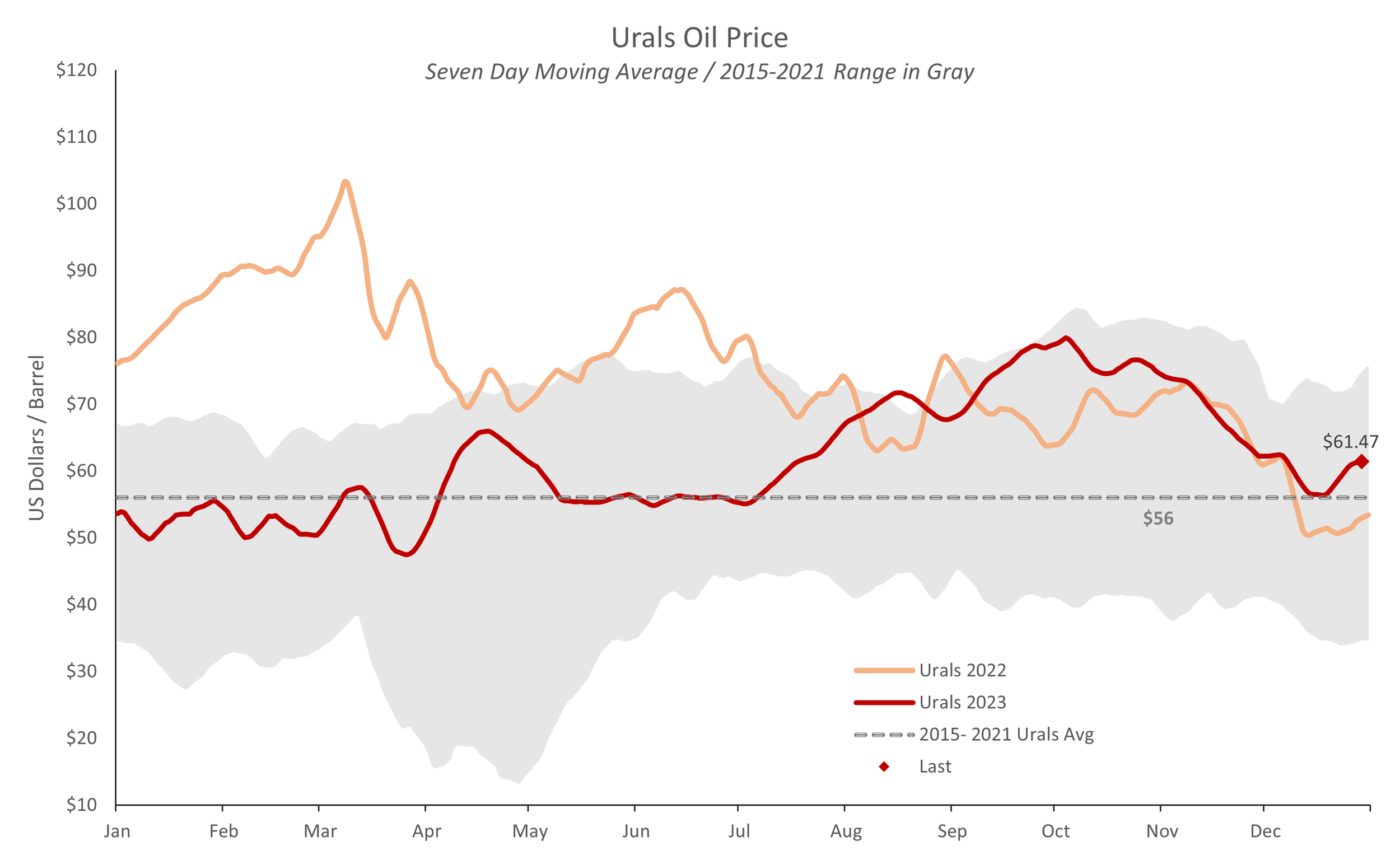

Price Cap, Ruble: Rebound of the Urals, Russia Coping

Oil Prices

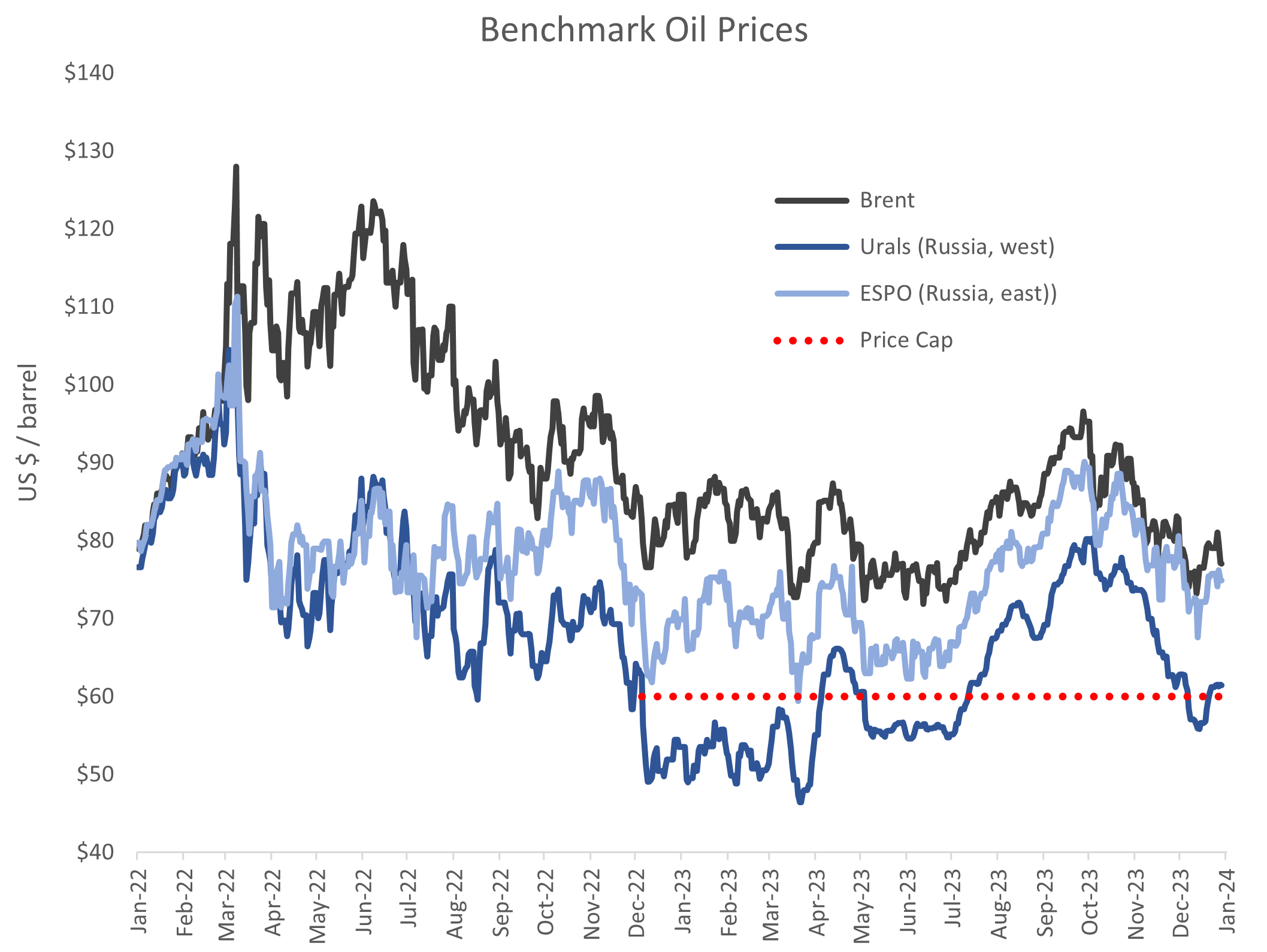

The oil price scene has been relatively uneventful in the last two months, with Brent loitering in the high-$70s to the low-$80s and dropping $6 last week alone to a tepid $77 / barrel on Friday.

Urals, Russia's western oil export price, has similarly been hanging around the Price Cap limit since early December, averaging $59.50 until the past week. Even as Brent was sliding, Urals has spiked up the past ten days, gaining $7 / barrel to close at just under $68 / barrel on Friday.

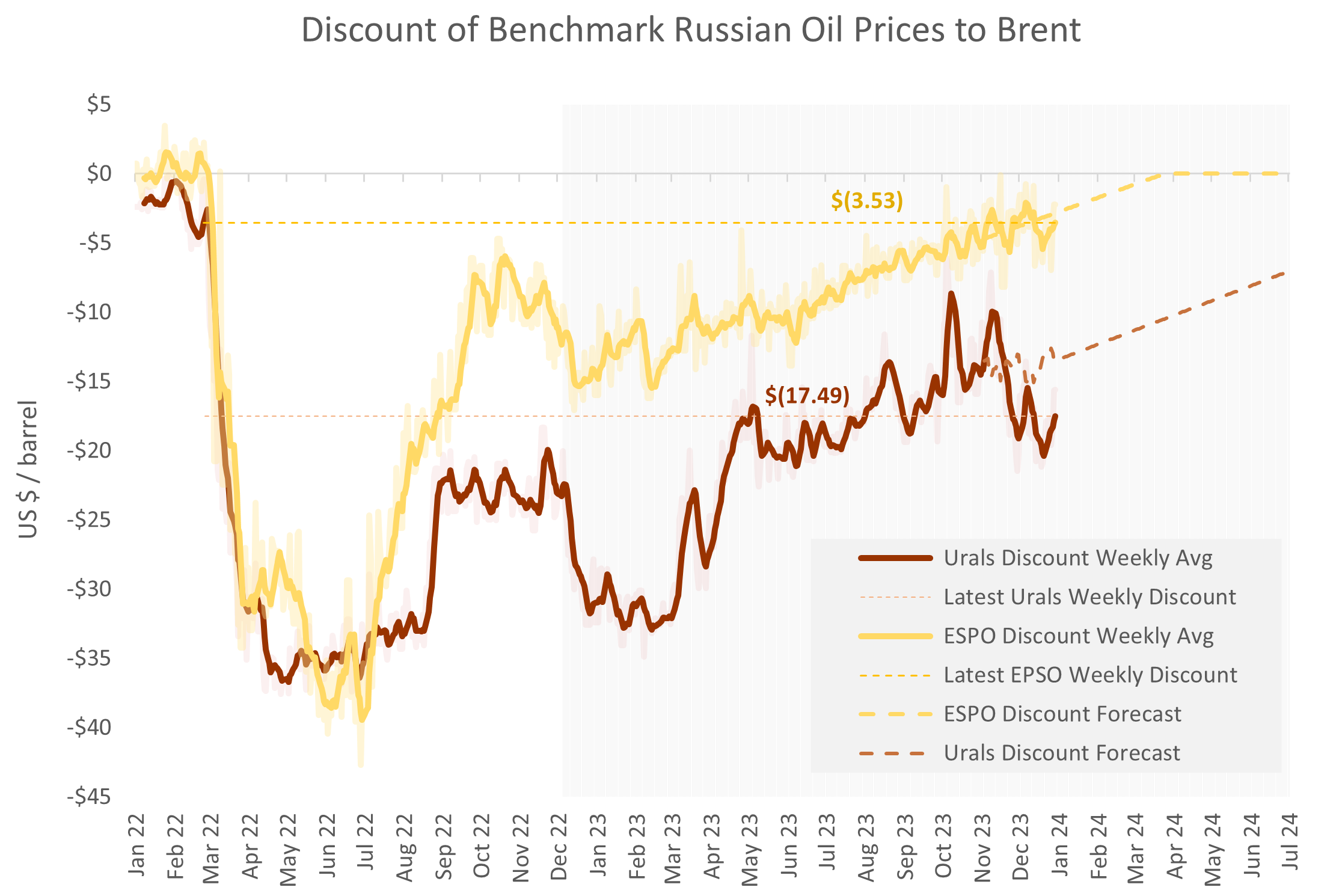

Accordingly, the Urals discount - the difference between the Urals price and Brent -- has narrowed, closing at $8.72 on Friday and averaging $13.19 / barrel for the week. This average is actually close to our forecast value of $12.62. Notwithstanding, the discount is probably understated as changes in Brent tend to be reflected only with a lag in Urals, and the drop in Brent will only be captured in the Urals price this coming week.

Still, it looks like the Urals discount is on the decline once again. This is not unexpected, as this sort of volatility is typical of black markets. The US stepped up Price Cap enforcement in November, and the discount widened as a result. A greater discount increases profits, and this induces the introduction of new players or new smuggling methods to the Russian oil trade. The resulting increase in demand then closes the discount once again.

This is the same dynamic which we see with illicit drug prices. A round of enforcement creates scarcity in the narcotics supply, which raises prices and profits, and stimulates innovation in smuggling practices. This in turn causes the Whac-a-Mole syndrome which we see in not only Russian oil smuggling, but also in drug smuggling and illegal immigration, the latter being the smuggling of illicit labor over the US southwest border. Because enforcement increases available profit margins to intermediaries like drug cartels or UAE shipping companies, enhanced enforcement is quite literally self-defeating, and a key reason why prohibitions are to be avoided as public policy. Every time one channel of smuggling is blocked, another appears somewhere else, with the authorities constantly chasing the smugglers' ever-changing tactics, just like the children below trying to whack the moles as they pop up.

The Urals price is not particularly high by recent standards, but is in fact the highest since 2015, excluding only the surge of 2022 at the start of the war.

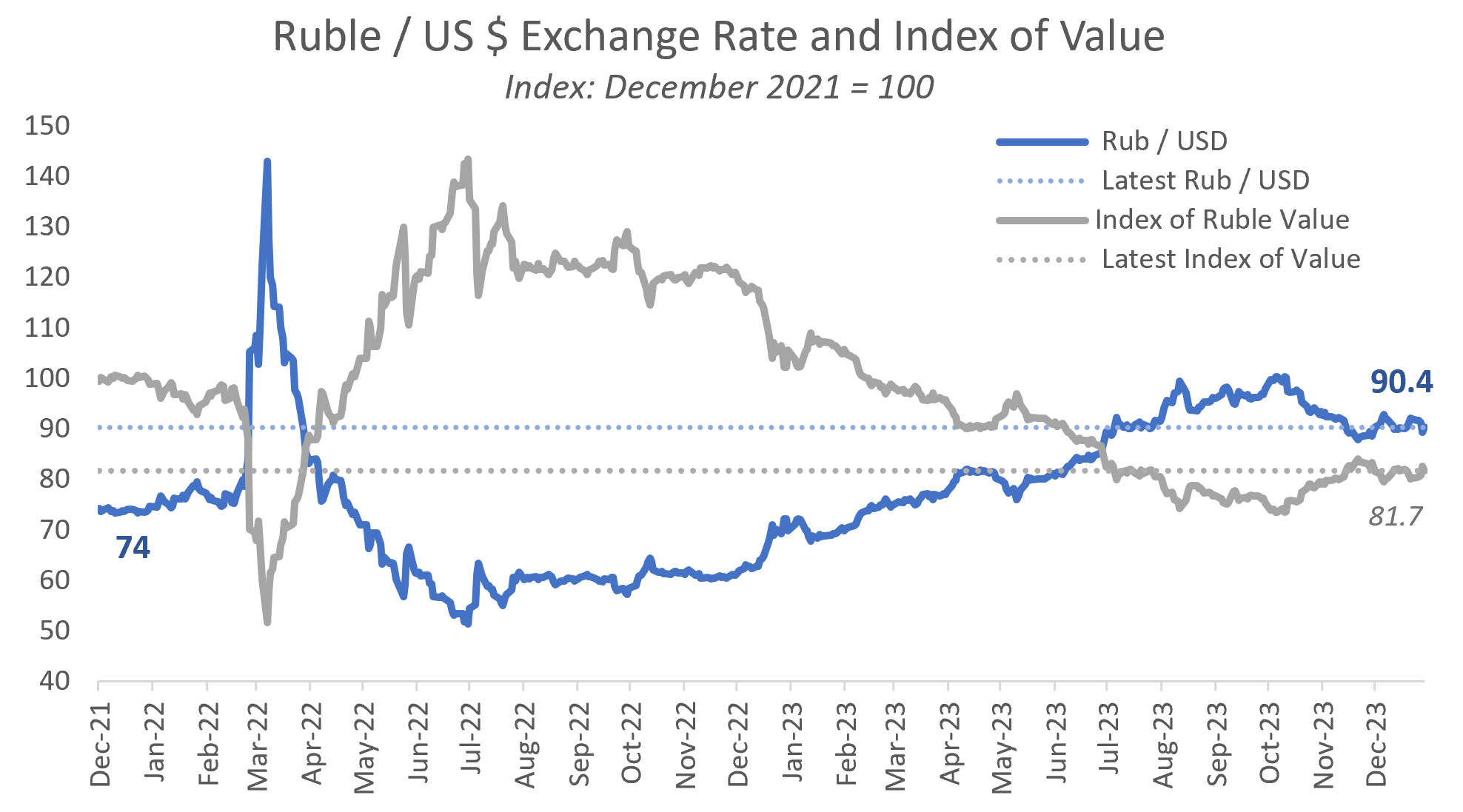

Ruble

Like Brent, the ruble has been largely range-bound since November, trading within a few points of 90 ruble / USD.

Russian money supply growth, as measured by M2, has been ebbing according to the statistics of the Russian central bank. Annual money supply growth in Russia reached 24% in 2022, but only 19% at the close of 2023. The Russian money supply from 2015 to 2021 grew by 10% annually on average. Thus, Russian M2 growth has substantially exceeded historical norms in the past two years, with the implication that accommodative monetary policy has been supporting the Russian economy, and by extension Russia's war effort, by the equivalent of $114 bn in 2022 and $71 bn in 2023. Russia's elevated interest rates, 16% from December, appear to be having the desired effect of reducing inflationary pressures. Moscow appears to be successfully adjusting policies, notably fiscal policies, to deal with the costs of the war.

Congressional Salaries should be $294,000

Sen. Elizabeth Warren (D, MA) has called for an increase in Congressional salaries. But what's the right number, and even more importantly, the right structure? Pay structure matters, because it is the key tool for ensuring good governance, including, for example, 'draining the swamp', addressing corruption in Ukraine, and capturing Russia's governance in the post-conflict world.

Many forms of analysis commonplace in the corporate world are virtually unknown in the US government and DC think tank circles, and this includes the use of comparables. In the private sector, when we try to establish the price of a good lacking a market -- Congressional salaries, for example -- we try to find a proxy. And, in fact, we have one: the starting salaries of first year associates in New York. Why this? Most legislators are lawyers by trade, and we -- or at least I -- would hope that the public would prefer the best and the brightest to become members of Congress. First year law associates in New York are the best and brightest of their year, typically from Ivy League universities, and their salaries are tied to the market for premium legal services in the US. Therefore, if we believe we would like to recruit top-line legal professionals to serve in Congress, then first year associate salaries are a plausible comparable. Helpfully, such salaries have been published for more than fifty years.

As the graph above shows, Congressional pay in the 1960s was twice the compensation of first year legal associates in New York. By the mid-80s, however, legal salaries were catching up to Congressional pay, with Congressmen earning around 1.2x that of a first year associate. After 2000, first year lawyers in Manhattan were earning as much as twenty-year Congressional veterans. Since Congressional salaries were frozen in 2009, the comparison has yearly deteriorated such that today a 65 year old Senator will earn only 71% of the pay of a first year New York lawyer with effectively no work experience. In fact, the Majority and Minority leaders in the House and Senate earn $52,000 (21%) less, and the Speaker of the House earns $21,000 (9%) less, than a first year lawyer in New York. This is frankly pathetic.

I would argue that a Senator should make considerably more than a first year lawyer, perhaps twice as much, but the political equilibrium seems to fall considerably lower. Even so, a Congressman should make at least 20% more than a first year lawyer, about the same ratio as in the 1980s. If we apply that metric, Congressional salaries should be set at $294,000 for 2024, a 70% increase over the current pay level.

Structure matters even more. The MAGA crowd wants to drain the swamp by changing personnel. But that's not how the professionals do it. If you want to change behavior, you change the way people are paid, specifically by tying pay to performance.

I have consulted for both the private and public sectors, and the differences are stark. In the private sector, it's about delivering a product that customers value more than it costs to produce. Efficiency and effectiveness are essential. By contrast, money is not currency in politics. Popularity and electability are. Cost/benefit analysis may motivate economists and the think tank world, but I have never seen it used in producing legislation. Instead, policy in the real world is about catering to the preconceptions of constituents, toeing the party line, and adherence to pre-cooked ideological positions. Politicians often talk about fraud and waste, and some governments are indeed run by criminals and incompetents. (Corruption is the handmaiden of incompetence, in my experience.) In general, however, I have found national level bureaucrats and staffers in DC to be well-educated, well-meaning and competent. I consider many of them to be kindred spirits and friends. The problem runs deeper. Monies are typically allocated in the political process with little to no regard for effectiveness or efficiency, and implementation is often painfully slow and bureaucratic. This may not matter when the government is small, but when the national budget is $6 trillion / year, as ours is, the difference between slightly better and slightly worse governance is easily $1 trillion / year. That's a lot of money.

Tying pay to performance is a means to inject some discipline into the system, to motivate lawmakers to use taxpayer funds carefully. I will not belabor the mechanics of such a program here. Such a program would, however, have the effect of tempering political rhetoric in Congress and encouraging cross-aisle cooperation. It's one thing to bad mouth your opponents when it's costless. But when your bonus depends on using money wisely, well, people find a way to cooperate. If you're a burn-it-to-the-ground MAGA Republican, the most revolutionary thing you could do is introduce a performance-based bonus. Democrats might have to go along with it. After all, they want a pay raise, too.

Oil Production Growth: Russia > USA

Our regular round-up of Russian oil production, prices and Price Cap enforcement. I would also highlight coverage of our previous post in the Washington Examiner, Biden ignoring Pentagon, defense spending at pre-World War II levels.

Russian and Global Oil Markets

The EIA's monthly Short-Term Energy Outlook, issued this past Tuesday, reports Russian oil production rising to 10.76 mbpd in December, up a bit over the prior month. This is an impressive 200,000 bpd higher than the EIA expected just three months ago and the fourth consecutive monthly rise in Russian oil production.

The EIA has meanwhile updated its annual forecast for US oil production. In essence, this sees US production materially flat from September 2023 through the first half of 2025.

In fact, Russian oil production growth has marginally exceeded that of the US since August.

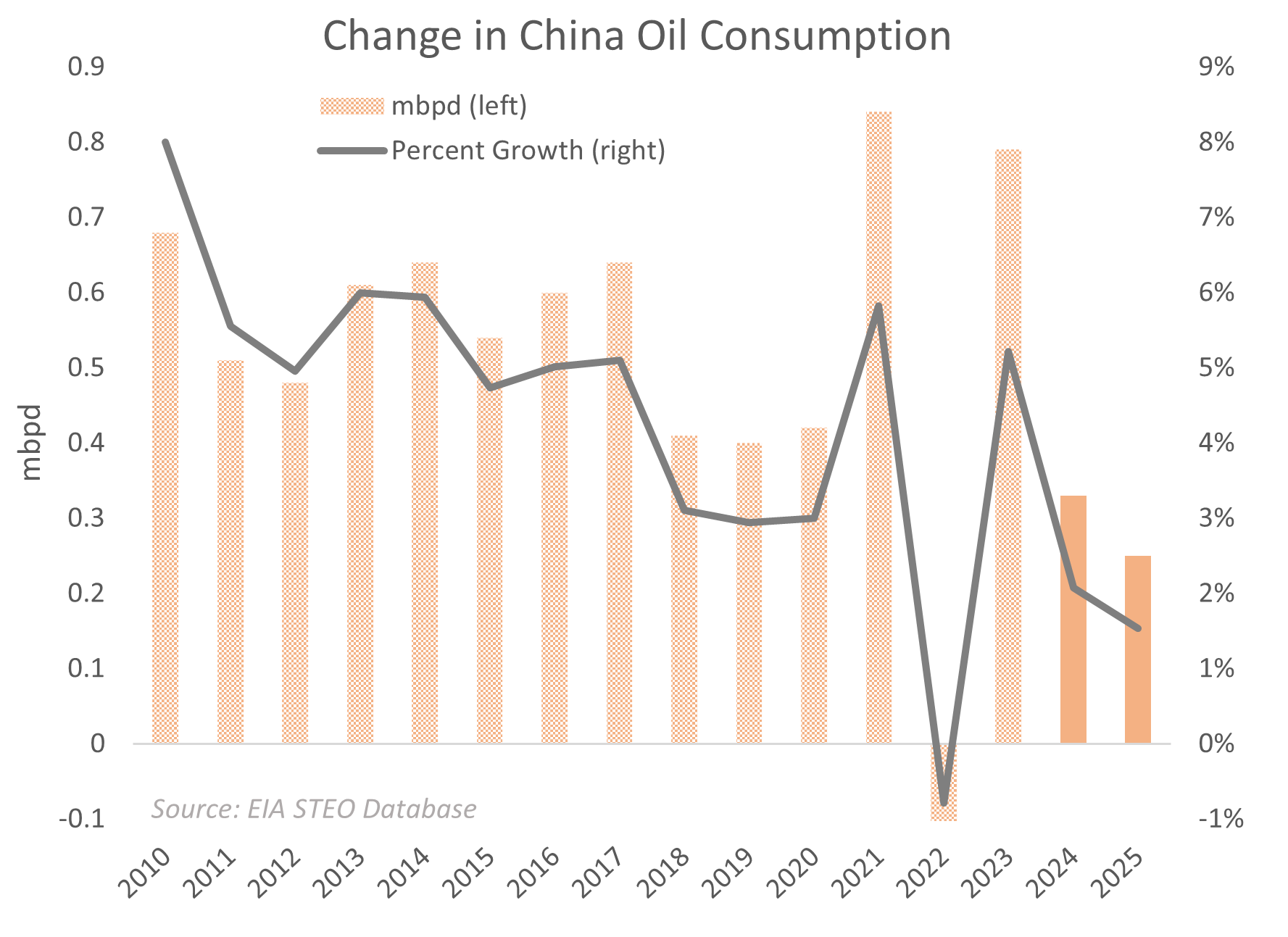

Flat US oil supply would ordinarily be bad news, as US shale oil production provided the discipline on oil prices for the last decade. However, two factors may mitigate the risk of an oil price surge. The first of these is weak anticipated demand growth from China. If all were well, we might expect annual oil demand growth of 3-5% or 0.5-0.7 million barrels per day / year (mbpd / year) in China. Nevertheless, the EIA anticipates growth of less than half this level, indeed, only 0.25 mbpd or 1.5% in 2025. This is consistent with the generally glum outlook for China.

Finally, OPEC is carrying surplus production capacity of approximately 2 mbpd over normal levels, and OPEC would ordinarily seek to deploy these reserves if the opportunity arose. Like weak Chinese demand, surplus capacity could act to suppress oil prices, which is good for Ukraine, as well as for the US and western Europe in aggregate.

Therefore, although plateauing US oil production would ordinarily be bullish for oil prices and negative for Ukraine, a poor outlook for China and ample OPEC production reserves suggest that oil prices could remain range-bound in 2024, and possibly beyond. On the whole, this appears positive for Ukraine.

Oil Prices

Brent closed on Friday at $78, largely in this range now for the last six weeks. A neutral price for Brent might be $82-87 / barrel, thus Brent would appear modestly below normal at present. Urals was similarly weak, closing Friday at $59, below the Cap limit for all of January to date.

Interestingly, the Urals discount, the difference between Russia's western oil export price and Brent, remains comparatively wide, averaging nearly $20 for the week. This is $6 greater than our forecast and suggestive of at least partial success in sanctions enforcement. Someone over at OFAC deserves a pat on the back for their sanctions work.

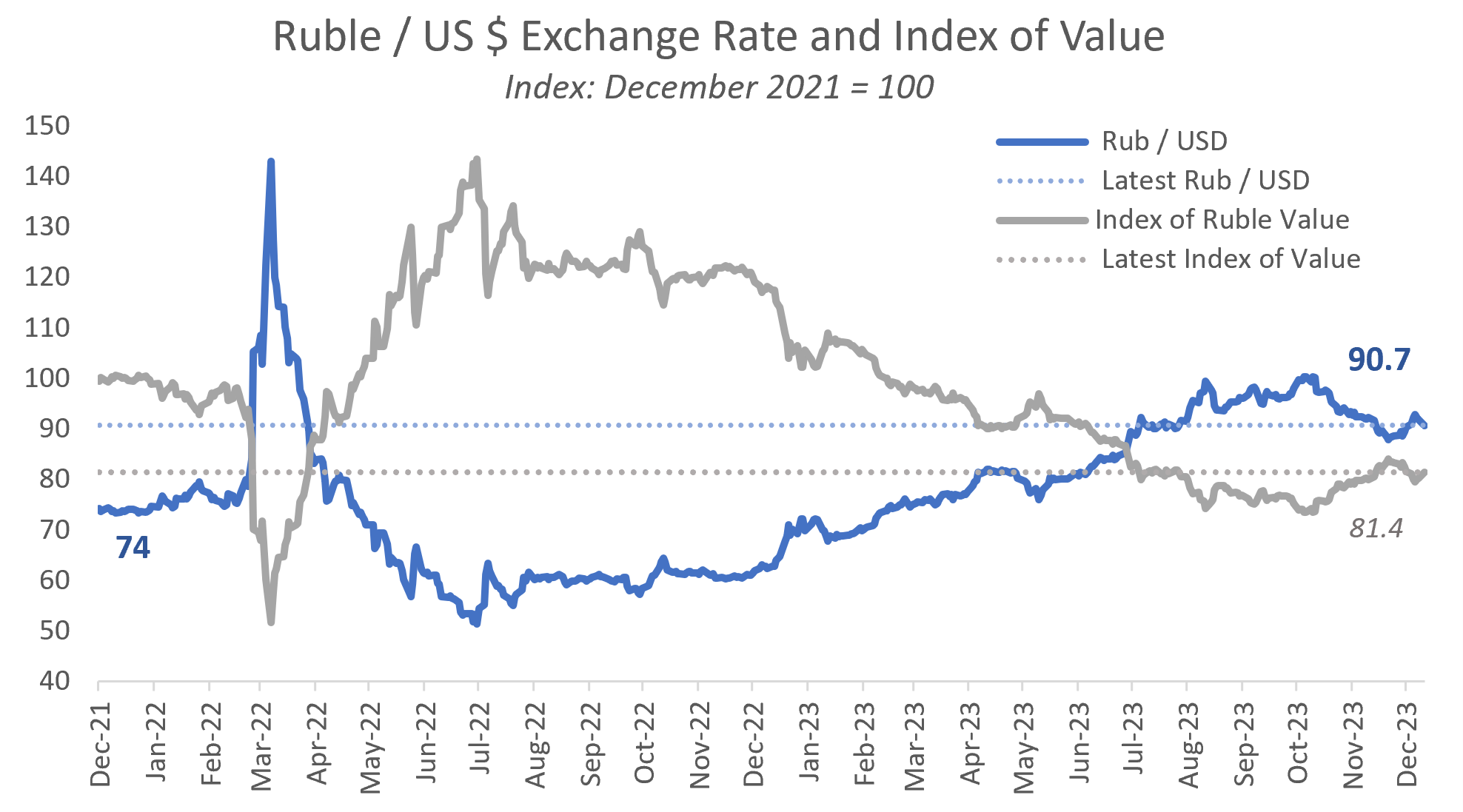

Ruble

The ruble appreciated marginally against the dollar this week, closing at 88 ruble / USD. This is largely unchanged in the last two months and contradicts recurring claims of a collapsing ruble.

Overall, oil prices remain favorable for Ukraine. We now need Congress to step up with some serious funding, notwithstanding fairly disastrous deficit numbers. Moreover, the Biden administration needs to refocus away from trying to seize Russian assets -- which are pretty well ring-fenced -- and instead restructure the Price Cap to capture the Urals discount and redirect this to Kyiv.

US defense spending below pre-war level, at historic lows

Reading the press, one might think US defense spending has reached astronomical heights. Take, for example, Barrons' latest piece on the topic, US Congress Passes Huge $886 Bn Defense Budget For 2024. One would think that the US is all-in for some cataclysmic battle.

Not even close.

Under the Biden administration, defense spending as a share of GDP has fallen to its lowest level since before World War II. The Fiscal Year 2024 Defense budget does raise spending as a share of GDP marginally, but to a level essentially tied for the lowest in the last 84 years with the 'peace dividend' during the Clinton administration. In fact, defense spending in 2024 will be a smaller share of GDP than it was before the Ukraine war began.

The comparison with earlier conflicts is even more stark.

During the Korean War (1950-1953), the US spent at peak 16% of GDP on defense, more than four times the current share.

During the latter stages of the Vietnam war, defense consumed 10% of GDP, three times the current level.

And during the Reagan administration, when the US was spending the Soviet Union into bankruptcy, defense outlays represented 7.6% of GDP, more than twice the current share.

Indeed, if we took the Ukraine war as seriously as the Korean war, then we would be willing to spend more than $4.4 trillion on defense, comfortably twice Russia's entire GDP.

Instead, US defense spending eroded to 3.6% of GDP in 2023 from a lowly 4.0% before the Ukraine war. The new defense budget raises spending marginally, to 3.8% of GDP, but remains the lowest share in the last 84 years, barring only the prior two years of the Biden administration.

Thus, given the perilous state of global security, defense spending stands at irresponsibly low levels and represents more mockery of, than commitment to, national security. To suggest that the US cannot afford to fund the war against Russia, that somehow we are tapped out and compelled to take a loss in Ukraine, is flatly untrue. Defense has been pathetically neglected under the Biden administration.

If I view the numbers as an analyst, a bump in defense spending to 4.6% of GDP looks warranted under the circumstances. This would represent an additional $225 bn in 2024 to prosecute the Ukraine war, among others.

Putin cannot match that. Russia's pre-war military budget was a mere $66 bn, rising to $140 bn for 2024, representing 35% of total government spending in Russia this year. Putin's discretionary war in Ukraine, one which he could stop tomorrow without harm to Russia, is squeezing out non-military programs, including social spending. The Russian public will not be happy.

This much is clear: The US is strong. Our military potential is not exhausted, it's untapped. It is our political potential which is exhausted. There is a lack of seriousness in Washington. The Biden administration appears to be playing at war rather than knuckling down and winning it. Meanwhile, Congressional Republicans seem ready to abandon national security. Behind all this is the notion that projecting weakness and indecision will translate into perceptions of strength and political popularity. If only our politicians show sufficient hesitation, lack of conviction and subservience to Moscow, US voters will love them. It's a model of leadership through capitulation.

President Reagan spent twice as much on defense as a share of GDP as we are, and Reagan did that at a time when we were not involved in a major conflict with the Soviet Union. This policy bankrupted the Soviet Union and represents one of the crowning achievements of the Reagan administration. We can easily do that again. A 1984 CIA analysis estimated the US economy at the time to be twice the size of the Soviet Union's. Today, the US economy is 5-14 times the size of Russia's, depending on the metric used. If the US is serious, Russia cannot keep pace, and Putin knows it.

It comes down to intent. President Biden may not be willing to lead on this. But House Speaker Mike Johnson can. If he says, "The US intends to prevail in Ukraine," and backs it up with some serious money, then we'll know where to find real leadership in Washington.

Wars: Korea vs. Ukraine

Rigs and Spreads Jan. 5: Steady rigs and imploding spreads

The rig and spread counts are seeing both regime change and seasonal variation

Horizontal oil rig counts appear to have stabilized in the mid 450s, essentially unchanged in the last two months.

This represents a new regime in the shale patch, as counts had been falling steadily throughout 2023

Frac spreads have rolled off heavily over the last four weeks, down 32 since early December.

Most of this can be attributed to seasonal factors, but the effect has been to stem the erosion in the DUC inventory witnessed over the last several years.

On seasonal trends, spread counts may be expected to recover over the next several weeks, leading to a renewed erosion in DUC inventories.

We continue to see a disparity between the EIA and media reports with respect to production growth.

The media frequently refers to surging US oil production, and that is certainly true considering 2023 as a whole.

However, the EIA sees US shale oil production peaking in October 2023, with modest declines to be expected over the next several months.

*****

Rig counts

Total oil rig counts: +1 to 501

Horizontal oil rig counts: +1 to 457

The Permian horizontal oil rig count: +3

The US horizontal oil rig count is rising at a pace of +0.5 / week

Frac spreads fell, -4 to 236, the lowest level in more than two years

DUC inventory, as measured in days of turnover, rose to 16.1 weeks on seasonal factors

Based on last year’s precedent, expect the spread count to recover and inventory to fall back towards 14 weeks

EIA PSR Week of Jan. 3: Modestly constructive

The EIA weekly report was modestly constructive.

Despite media reports of a ‘surge’ in product inventories, these are entirely normal when considering seasonality and demand factors. Crude inventories are similarly normal.

Gasoline and diesel supplied (consumption) look quite healthy, both up and reflecting greater affordability at the pump. The US consumer is feeling in a better mood.

Incentive-to-store analysis suggests that balances may remain relatively soft in the first half of the year, with gradual tightening through 2024. This suggests comparatively subdued oil prices through Q1, but with a gradual rise towards the back end of the year. Bear in mind this is current market sentiment, not necessarily a forecast.

US oil production declined 0.1 mbpd to 13.2 mbpd but is essentially flat over the last three months. This is consistent with the EIA’s monthly STEO, which sees US production on a brief plateau and then declining modestly to a lower level through Q3.

Notwithstanding, the Brent Spread (Brent – WTI) remains reasonably wide, $5.50 / barrel at writing. This is consistent, as before, with US production growth of around 800 kbpd / year. Lively US demand and flat US production growth should be driving higher oil prices, but it’s not. Maybe it’s China, or perhaps production growth is not fully captured in the data.

Overall, the report speaks to a healthy economy and balanced inventories, with a suggestion that production growth is better than the numbers say.

The Price Cap at Year End

Paul Bedard at the Washington Examiner kindly ran a piece based on my last post, here. Paul has covered my work on illegal immigration for the last several years, now preempted by my more immediate concerns with the Ukraine conflict. Also, find my editorials in Kyiv Post here.

Oil Prices

Brent closed the year at $77 / barrel, and Urals posted $61.47. Urals is marginally above the Cap limit of $60, but still well off the $71 / barrel the Russian government is budgeting to fund increased war spending in Ukraine. For now, this is positive for Ukraine.

The Urals discount -- the difference between Russia's western crude oil export price and the European benchmark Brent -- closed a bit to $17.50 last Friday. This is $4 / barrel larger than our Brent price-adjusted forecast of $13.50. (The Urals discount varies with, among others, the price of Brent. The discount narrows by about $0.25 / barrel for every $1 gain in Brent. Thus, if Brent rose from its current $77 / barrel to $87, we would expect the discount to narrow by $2.50 / barrel for this reason alone. I'd note this is a low-confidence relationship with an R2 of only 0.11 on a 0.0-1.0 scale. Take it as a rule of thumb, not as a rule.)

Once again, US enforcement seems to be producing some limited effect. The discount is back in the range seen in June and July 2023, but much improved from the tight spread in October and November. Thus, enhanced US Price Cap enforcement appears to have widened the discount, but only back to the levels which prevailed before October and November. Still, it's better than nothing and positive for Ukraine overall.

Urals ended the year about $8 / barrel higher than a year ago.

Ruble Exchange Rate

Finally, the ruble ended the year at 90.4 ruble / US dollar, largely unchanged in the last two months.

The war is settling into a kind of deadly monotony and routine, and that's visible in the statistics as well.

The war could end in '24

With the close of the year, it is once again time to reconsider the prospects for the end of the war. The major change, compared to our earlier analysis, is the elevated pace of Russian casualties. During November and December, the Russians lost just shy of 1,000 men per day, according to the official Ukrainian count. This is a spectacular pace of loss and, if continued, could shorten the war by as much as a year.

The length of wars is determined by a number of factors. These include the belligerents' economic and military capabilities, as well as their ability to maintain political cohesion. Military deaths are a key factor in the public's willingness to sustain a conflict. Prior wars can therefore provide some insight into the limits of, in this case, Russian perseverance. The current Russo-Ukrainian war already qualifies as the fourth deadliest external conflict in Russian history. The third is the Crimean War (1853-1856), which lasted 900 days and cost the Russians 450,000 dead in a losing effort. At the recent pace of Russian losses, the current conflict will move into third place before Easter. It is worth noting, however, that the population of the 1850s Russian Empire was approximately half of its current level. Therefore, adjusted for population, Russian eliminations would need to rise to 900,000 for the current conflict to qualify as third worst of all time and, by historical precedent, induce Russian capitulation.

At the lower limit, Moscow might plausibly face meaningful public resistance around 650,000 Russian military deaths, about twice the current number and half again as much as from the Crimean War of 1853. This view is based on three factors. First, deaths are simply more visible today, even with the various censorship programs employed by the Russian government. Second, Russia is for all that a marginally more civilized country than it was in the 1800s, and the public's tolerance may be accordingly less. Third, and most importantly, this war is entirely discretionary for Russia. Unlike World War I, which saw massive losses of Russian territory, including Finland, Poland, the Baltics and Bessarabia (largely today's Moldova), Russia is facing no territorial losses compared to the pre-war era. Further, no fighting is occurring on Russian soil and no one has attacked Russia. The war poses no existential threat to Russia as did, for example, the German invasion during World War II. St. Petersburg is not under siege, no one has sacked Moscow, and there is no house-to-house, to-the-death fighting in Stalingrad (Volgograd today). Thus, the Kremlin must justify 650,000 deaths for what was supposed to be a mere three-day, special military operation entirely of Putin's choosing. Russia's Achilles heel is exactly the low stakes of the conflict. Putin could order the troops home tomorrow, and Russia would be no worse off than in 2014, a time when Russia was actually seeing something of a renaissance.

At the current pace, Russian losses will reach 650,000 dead by late 2024. If this proves to represent a threshold of public tolerance, the war could end at that time. The next stop is one million Russian dead, which could be expected by autumn 2025 at the current rate of eliminations. If the war extends so far, it will have lasted as long as World War I for Russia, and the media will routinely compare the conflict to the Great War, which saw 1.8 million Russian military killed (1.5 million adjusted for Russia's current population). Although Putin claims Russia will fight for five years, the Russian public found the losses of World War I intolerable and overthrew their government. If Russia continues to lose 1,000 soldiers every day, Russia will likely concede the war before the end of 2025.

For Americans, there are some important takeaways.

First, this is a major war. It will rank third in all of Russia's bloody history by the time the tulips bloom this spring. This is not some minor conflict in a faraway country, but a major European conflict requiring substantial determination and commitment.

Second, this is not a forever war. It will be resolved in some fashion within two years if hostilities remain at their current pitch.

Finally, independence is worth a very large number of Ukrainian lives. The outcome of this war will likely determine the fate of Ukraine — and Europe — for the next century, just as the defeat of the Ukrainian struggle for independence in 1917 determined Ukraine's narrative until the fall of the Soviet Union in 1991. The Bolshevik defeat of Ukraine's republic set the stage for the Holodomor, which claimed up to 5 million Ukrainian lives, and presaged the Soviet domination of Eastern Europe for a half century.

The Ukrainians need to decide what independence is worth. If I compare it to Hungary, from which my family fled in the closing days of World War II, we would have gladly fought and thought losses of two percent of the population worth it if Hungary could have retained its independence in 1945 or regained it in 1956. That equates to nearly one million Ukrainians, and at the current rate of exchange, 3-5 million Russians. If it is worth the price to Ukrainians, the Russians will lose, as long as Ukraine's allies stand beside it.

Urals below Cap; Some success with enforcement; Let's stop pussyfooting around

Russian Oil Prices

Brent continued to drift downwards this past week, just under $76 / barrel at writing. Urals accordingly fell, just under $57 on Monday, its lowest since July and now below the $60 Cap threshold. All this is good for Ukraine.

Some analysts believe oil prices have found a floor. Copper prices, another proxy for the state of the global economy, suggest Brent should be priced around $84. Nevertheless, questions linger over the health of the Chinese economy and whether US oil production growth is understated. Analysts seem a bit perplexed overall, and that includes this one. More on this when the EIA publishes its monthly statistics later this week.

The Urals Discount, the difference between Russia's western crude export price and Brent, has widened to $17 for the past week as a whole. This contrasts with our forecast of $12 / barrel, implying that recent sanctions against UAE shippers have had an effect worth about $5 / barrel. The Biden administration can bank this as a modest, short-term win, but a win nevertheless.

For doubters, I would note that the ESPO discount, the difference between Russia's eastern oil export price and Brent, is closing faster than our forecast, posting at $3 / barrel versus our forecast of $3.40 / barrel for the week. Russia's eastern sales are not substantively subject to the Price Cap, so the divergence between a shrinking ESPO discount and a growing Urals discount can be attributed to enhanced enforcement in the Urals zone. Again, a small but useful win for the Biden administration.

The ruble has crept up to 91 / USD and showing a slight weakening trend attributable to softer Brent, and hence Urals, oil prices in the last few weeks. Again, this is good for Ukraine.

As noted above, the Urals oil price is about the same as last year and essentially the same as Russia's average export oil prices from 2015 to 2021. Overall, this is a positive for Ukraine, as it makes higher military spending more problematic for the Kremlin.

Reluctance to Fund Ukraine

Ukraine's allies are beginning to show an indifference to the fate of that country. This needs to be remedied, but should not be surprising.

It's a slough

The US public struggles to grasp the scale of the conflict. Americans have come to expect the US to crush its adversaries in a matter of weeks without material sacrifice or anguish for the country as a whole. Such was the case with the first and second Gulf wars, the invasion of Afghanistan, and various smaller conflicts spanning the last forty years. The Israelis are mopping up Hamas in just such a style.

Ukraine is different. By population, Russia remains by far the largest country in Europe and, despite its incompetence on the field, can still muster a large army with a vast, if unimpressive, array of weaponry. The battlefield in Ukraine has come to resemble the fronts of World War I, where vast sacrifices of men and materiel yielded minimal changes on the ground. The conflict has devolved into a monotony of death, where 1,000 casualties per day are no longer newsworthy and footage of tanks and artillery exploding have become just more of the same. Under the circumstances, the average American wants it all to end. That's particularly true of a war in a far away country with its own checkered past.

It's the economy, stupid! (Sort of.)

The reluctance of the US and European public is not just a matter of emotions. A recent Bankrate survey shows that, by a margin of 2-to-1, employed Americans feel that their wages are not keeping up with inflation. Thus, despite robust recent GDP growth and near full employment in the US, Americans are largely unhappy with the economy. Although funding the Ukraine war is not material in the overall US economic picture, it nevertheless represents to many an extravagant outlay on a discretionary war at a time when they feel their own budgets are pinched.

The public mood is affecting the political landscape. An NBC News poll from September found the GOP advantage on the economy to be the highest recorded in more than three decades of NBC News polling. Ukraine funding is part of that, and it is affecting the attitude of political leadership.

Isolationism

Finally, the US has traditionally had a strong isolationist streak. For example, as late as September 1940 -- a year after the fall of Poland, after the capitulation of France and well into the Battle of Britain -- only a bare 52% of Americans believed the United States ought to risk war with Germany to help the British. Britain and France are far closer to Americans' hearts than Ukraine will ever be, and yet Americans were all but unwilling to lift a finger to help our core European allies before Pearl Harbor ended the debate.

All these factors matter in the US. They need not paralyze policy, but they need to be understood, respected and addressed.

Three Takeaways

Biden needs to lead

The war in Ukraine is attributable to a failure of deterrence by the Biden administration. The disastrous pullout from Afghanistan marked President Biden as a weak leader and encouraged President Putin to try his hand at Ukraine. When Biden declined to deter Russia with promises of direct military assistance to Ukraine, Putin again felt he had a green light to invade. Only when public opinion nevertheless demanded that the US government support Ukraine did the Biden administration take a stand, but even then slow-played the provision of arms and other support, allowing the Russians to entrench and deliver the stalemate which now prevails. In addition, the on-going vacillation in US policy fuels the current Russian onslaught in Ukraine.

If the Republicans are reluctant to fund the war, well, President Biden has given them leeway to do so. Instead, the President should stand up and declare that the US intends to see the war through to victory. If the Republicans want to champion a loss in Ukraine, let them own it. If Republicans want to run on 'I'm the guy who lost to the Russians', let them run on it. The Republicans are rapidly getting used to losing elections they should win. But if the President thinks vacillation will win him political support, it won't. It will only reinforce a view of him as a weak leader. Biden needs to stand up and clearly declare that the US is playing to win.

The Republicans need to get serious

On the face of it. Ukraine's position vis-à-vis Russia looks dire. The IMF estimates Ukraine's GDP, as measured in current US dollars, to be only 9% that of Russia, and the situation is not expected to change materially in the future. As a result, Russia can afford to spend more on the war. A lot more. Russia's planned 2024 military expenditure more than doubles from pre-war levels to $109 bn for 2024. This is more than Ukraine's entire GDP. Barring a reform of the Price Cap, Russia can sustain this level of spending indefinitely. Without external support, Ukraine's long-term position looks dire indeed.

However, the matter looks quite different in the broader context. While Russia's economy is large compared to Ukraine's, it is chump change compared to the US economy, which is 14 times larger as measured by current US dollar GDP. The comparison is even more ridiculous if Ukraine's broader set of allies is included, which together with the US, have a GDP 27 times that of Russia. The notion that the US and Europe are somehow unable to keep pace with Russian military spending is absurd on the face of it. This is the equivalent of a 270 lb. man being afraid of a 10 lb. child. Indeed, the IMF projects the US economy to add the equivalent of two Russias to 2028.

The question is whether Republican leadership intends to lose to a Russia which qualifies not as the high school varsity team, not as the junior varsity, but as the eighth grade pick-up team. Does House Speaker Johnson really intend to be remembered as the guy who lost to the eighth graders? One would hope not. It's time to stop fooling around and get back in the game.

None of this should be construed as antipathy to many Republican objectives, including accountability for Ukraine funding and reinstating border control. No one has garnered more coverage in the right media than I have regarding the border, and no one has been more critical of administration border policy than I have. Notwithstanding, it's time to stop fooling around with Ukraine's funding.

Beating the Russians

Beating the Russians requires men, money and materiel. Of these, money is arguably the most important, for it buys men and materiel. A key means to beat the Russians, therefore, is to have more money, and that involves contributing more of one's own and taking the Russians' money away.

Russia's defense spending, as noted above, more than doubles its pre-war level to $109 bn in 2024, versus $48.2 bn in 2021. The pre-war budget was funded by Russian oil export prices averaging $56 / barrel from 2015 to 2021. The Russians are budgeting Urals at $71 / barrel for 2024, which, augmented by a higher ESPO price, provides an incremental $48 bn for the Russian government in 2024 and thereby funds the lion's share of Moscow's surge in military spending.

Of this, more than $30 bn can be seized from the Russians, even at today's low Brent and Urals price. Once Russian oil revenues are redirected to Ukraine, the entire calculus changes for Moscow. Its available resources will be trimmed, requiring deeper spending cuts to social programs or higher inflation, or both. Add to that 1,000 eliminated Russians every day, and the war will prove untenable over time, even as the funding support from the US and other allies remains tolerable from the perspective of domestic politics.

As a conceptual matter, beating Russia is not particularly hard. We have a bigger stack of chips at the poker table. A much, much bigger stack. With that, our strategy comes down to a predictable call-and-raise. Whatever the Russians put in, we put in more. And if we want to save money, we reach across the table and take the Russians chips away from them.

Right now, we need policy that is steady and confident, with the awareness that we are the big boy at the table. It will still be a long war, but we can easily regain the upper hand.

Rigs and Spreads Dec. 1: Nice adds

Horizontal rig counts rose by 6 this past week, closing the best four week stretch in a year. WTI at $90 appears sufficient to bring incremental rigs into operation. Alas, oil prices have been dropping for the last several weeks, and while we may still see rig gains next week, counts should start to fall as we head towards year-end. Indeed, they should fall at a fairly rapid pace into January, assuming our breakeven analysis holds up.

Rig counts

Total oil rig counts: +5 to 505

Horizontal oil rig counts: +6 to 457

The Permian horizontal oil rig count: +3

The US horizontal oil rig count is rising at a pace of +3.50 / week, the best in a year

Frac spreads fell, -5 to 276

DUC inventory, as measured in days of turnover, fell to a new low of 12.4 weeks

More rebalancing of the rig-to-spread ratio is required; this week is suggestive of trends to come, with rigs rising and spreads falling

The Brent Spread (Brent – WTI) remains near $5 / barrel, suggesting US production growth remains solid

EIA PSR Week of Nov. 24: The data's buggy

Excess crude and key product inventories are normal when allowing for seasonality and demand.

Gasoline and diesel supplied (consumption) look suspiciously low and product exports appear unusually high, but otherwise, the picture is as it has been on the consumption side, with refined product consumption running about 5% below normal.

Incentive-to-store analysis shows that market sentiment has been absolutely crazy over the last month and a half. On Sept. 27, the market perceived a huge crude supply deficit. This has reversed into the current modest surplus, per our analysis of the futures curve. This really should not happen, but clearly, it has.

US oil production remains flat at 13.2 mbpd, as it has been for the last eight weeks. I cannot find a similar eight week stretch in the data, which suggests that the EIA is winging it, as the EIA’s new software upgrades remain unreliable in reporting production.

The Brent Spread (Brent – WTI) has widened to $5 / barrel, which is normally consistent with US production growth of around 800 kbpd / year. US production growth is likely under-estimated, possibly materially so.

Overall, the EIA’s software upgrade remains buggy. The missing barrel count (red circle, the difference between the light and dark blue lines, graph above), instead of declining as the EIA had no doubt hoped (green circle), has exploded, and seemingly in a cumulative fashion. This is not unusual for software modifications, particularly in such rich, data-intensive and near-real-time systems as the EIA uses. It’s really the 8th wonder of the world, but the EIA will require a few weeks to iron out the kinks. Take the data with a grain of salt in the interim.

Urals weaker; Ruble stronger; UAE mischief; Danish grit

Russia Oil Prices

Brent has settled into the low $80s, closing on Wednesday at $82 / barrel. Urals tracked Brent with a few days' lag, closing at $65 mid-week. Urals is $9 / barrel above the 2015-2021 average and $5 above the Price Cap. This is good for Ukraine, as last week.

Oil demand depends upon the state of the global economy. The US economy is unwinding pandemic fiscal and monetary policy, and prices of a number of goods are falling, yet remain well above their pre-pandemic level. The question is therefore whether the US sees a 'soft landing' with the economy returning to pre-covid levels, or whether it overshoots into a recession. The price of oil will depend heavily on which version proves out. Moreover, China's economic prospects remain uncertain, and we might expect a financial crash there as the country transitions from a high growth to a lower growth regime. But when?

US shale production set the price of oil from mid-2014 until December 2021, and still remains a key constraint on oil price increases. The EIA has called peak US oil production for this past August, but statistical analysis suggests production growth may be higher than thought. The EIA has revised US production up by about 1 mbpd since the summer, and another material revision would come as no surprise. If US production is growing faster than believed, then oil prices could be quite a bit softer, at least for a few more months.

Thus, we have a fair amount of uncertainty on both the oil demand and supply side, none of which should influence appropriate policy regarding the Price Cap -- although reforming the Cap would be easier in a lower oil price environment.

As we forecast last week, the Urals Discount, the difference between the Urals and Brent oil prices, widened again this week, on Wednesday reaching $14.69 / barrel for the week as a whole. The ESPO discount also widened, but is now under $4 / barrel. China has agreed to work with the US on certain matters, and opening the ESPO discount wider should be on the table, as a discount of a measly $4 is less than the difference between Brent and WTI.

Ruble

The ruble continues to appreciate against the dollar, closing at 88.4 ruble / USD on Wednesday, likely buoyed by high oil prices during the last month or two. If Brent stays weak for any period of time, expect the ruble to slip back into the 90s.

The US Treasury sanctions UAE Mischief

The US Treasury sanctioned three UAE-based companies for shipping oil above the $60 / barrel cap. The Treasury details the penalties:

[All] property and interests in property of the [sanctioned] persons above that are in the United States ... are blocked, [as are] any entities that are owned ... by one or more blocked persons. These prohibitions include the making of any contribution or provision of funds, goods, or services by, to, or for the benefit of any blocked person and the receipt of any contribution or provision of funds, goods, or services from any such person.

The respective shipping companies are short-lived, special purpose vehicles chartering the tankers in question. It is fair to assume that these shell companies have no assets in the US and that the owners, if they can be identified at all, are either strawmen or have no interests in the US. The Treasury precludes these companies from using US suppliers. This principally matters for insurance, and that is primarily British. If British insurance is unavailable, these shipping companies can use Russian insurance. Thus, Treasury sanctions look largely toothless and symbolic. This is typical of prohibition enforcement.

The UAE is more broadly a hub for Price Cap evasion and serves as a case study of the black markets, corruption, and the antagonistic behavior which arises as a result of prohibitions. More on this in a separate post.

Danes show some Grit

The Financial Times reports that "Denmark would target tankers transiting the Danish straits without western insurance, under laws permitting states to check vessels they fear pose environmental threats." This must have come from the Danes themselves, and it is a welcome display of initiative and determination. Of course, the proposal was torpedoed as soon as it was launched, as black market theory predicts. Prohibitions attempt to prevent willing buyers from transacting with willing sellers, and the Danish initiative would prevent those willing buyers, indirectly the G7 countries, from acquiring needed oil. Therefore, the proposed interdiction never saw the light of day, as we would expect.

Nevertheless, this is very much the right idea. It cannot. however, be enforced in the form of a prohibition. Black market theory makes that plain enough. But there are better alternatives.

Rigs and Spreads Nov. 17: Rig and spread gains within overall steadiness

The breakeven to add US horizontal oil rigs now exceeds $90 / barrel WTI. That is, at $90 WTI, we can expect US operators to be cutting rigs. That is incredible by the standards of the last decade, when analysts like Goldman Sachs spoke of $30-40 breakevens.

Rig counts are essentially holding steady over the last five weeks

Total oil rig counts: +6 to 500

Horizontal oil rig counts: +6 to 452

The Permian horizontal oil rig count: +5, the biggest gain since February

The Canadian horizontal oil rig count eased back this week, -4 to 119, now 10 below this week last year

The US horizontal oil rig count is rising at a pace of +0.75 / week on a 4 wma basis.

This number is positive for the third time in the last 50 weeks

Frac spreads rose, +8 to 276

DUC inventory, as measured in days of turnover, fell to a new low of 12.8 weeks

Since July 2020, 16% of completions have come from cannibalization of DUC inventory

The Brent Spread (Brent – WTI) remains open, suggesting US shale oil production is exceeding expectations.

This is also true if we consider US production including unaccounted-for barrels, which continues to suggest production growth in the 600-800 kbpd / year pace

Ukraine Funding: The Price Cap and Illegal Immigration are the Same Problem

Russian Oil Prices

Brent continued to unravel last week, closing on Friday at $81. Accordingly, Urals has also fallen just below $70 for the first time in two months. A lower Urals price is good for Ukraine, although it remains well clear of the $60 Price Cap.

The Urals discount -- the difference between Brent and Russia's western crude oil export price -- narrowed to $10.00 / barrel last week, but this is likely an artefact of reporting disparities between Brent and Urals. Expect the discount to widen to $13.50 as Brent stabilizes.

The EIA issued its November estimate of Russian oil production this past week. The Russian oil supply has been revised up 0.1 mbpd across the board starting in September 2022. Such revisions are not unusual for the EIA and are minimal considering uncertainties about Russian oil production during this wartime period. At 10.6 mbpd, Russia's October oil production was 7% below its pre-war output and 11% below the EIA's pre-war forecast for the month of October. As last month, the EIA expects no further reductions in Russian oil output, and indeed, sees Russian supply increasing by 0.15 mbpd (+1.4%) heading into 2024.

The Price Cap and Illegal Immigration

The new Speaker of the House, Mike Johnson (R, La), finds himself in a precarious situation. On Saturday, he unveiled a proposal to avoid a partial government shutdown by extending government funding for various programs until Jan. 19 and Feb. 2, according to the Associated Press. The bill excludes the funding for Israel and Ukraine which the Biden administration has requested. Johnson defended the bill as placing the "conference in the best position to fight for fiscal responsibility, oversight over Ukraine aid, and meaningful policy changes at our Southern border.”

Thus, funding for Ukraine has become intertwined with illegal immigration. Since evading the Price Cap and illegal immigration are the same problem in economic terms -- both are black markets -- they can be addressed with similar approaches.

Black markets arise as a result of prohibitions. A prohibition occurs when a government attempts to prevent willing buyers from transacting with willing sellers at market prices. Illegal immigration exists because the demand for US work visas is vastly greater than the supply of those visas at the offered price of $190. Therefore, unskilled labor from Latin America and elsewhere has an incentive to jump the US border, knowing that willing buyers -- US businesses -- are waiting to purchase the migrants' labor at 4-7x the wages of their home countries. That's illegal immigration in a nutshell.

The Embargo and Price Cap on Russian oil are essentially similar. The Russians want to sell, and global refiners want to buy, Russian crude at market prices. The Embargo and Price Cap are intended to prevent such transactions. Neither has succeeded. The Embargo has led to a simple restructuring of oil trade flows, with India, China and Turkey replacing Europe as Russia's primary export market. Similarly, the Price Cap has motivated Russia to circumvent such controls, for example, by the establishment of its own 'shadow fleet' of tankers and fraudulent declarations by market participants regarding agreed oil prices. This was entirely predictable, as enforcement-based approaches fail almost without exception, regardless of the product, country or historical period.

The US does, however, have three examples of success in ending black markets: the repeal of Prohibition for alcohol; the legalization of gambling; and the partial and halting legalization of marijuana. This is not the place to dwell on particulars, but the graph below illustrates the potential of the legalize-and-tax approach. In Fiscal Year 2023, border apprehensions of illegal immigrants were running six times the level of the Obama administration, and Border Patrol seizures of hard drugs like cocaine, heroin and fentanyl were twice their Obama-era level. By contrast, Border Patrol seizures of marijuana at the southwest border are running at 1.8% -- that's right, 1/55th -- of the level of the Obama administration. Smuggling of cannabis over the Mexican border has all but ended, and in fact, today the US is a net smuggler of marijuana into Mexico by value. That's the power of the legalize-and-tax approach, and we can use it to both close the border to illegal immigration and reform the Price Cap.

If the Speaker and the Republican conference are looking for alternatives, a legalize-and-tax approach can work for both border control and Ukraine funding.

The Republicans can require the Biden administration to begin a formal assessment of a legalize-and-tax approach to border control. This would avoid creating an obstacle to passage of a Continuing Resolution while initiating the first, crucial step towards ending illegal immigration using the proven, textbook approach. President Biden can agree to such a proposal, for it would help his re-election prospects as well. I would note that the legalize-and-tax approach to end illegal immigration has been endorsed by the Washington Examiner and received constructive support from the likes of Breitbart and the Epoch Times. The hard right is willing to take a look, and that should provide some comfort to Republicans as they consider options.

Meanwhile, Republican requirements for oversight of Ukraine spending are far too modest. The principal goal should not be Ukrainian accountability (although this is desirable), but rather making the Russians pay for the war, and not only the war, but Ukraine's reconstruction and the full spectrum costs incurred by the US and Ukraine's allies for the conflict. It's not about ensuring US taxpayer money is well spent; it's about making sure the taxpayers get their money back.

General George Patton, America's most prominent general of World War II, once famously declared, "No bastard ever won a war by dying for his country. He won it by making the other poor dumb bastard die for his country." A legalize-and-tax approach can make the other poor dumb bastard pay for the war. That's something Democrats and Republicans can both support.

Rigs and Spreads Nov. 11: Breakevens above $90!

The breakeven to add US horizontal oil rigs now exceeds $90 / barrel WTI. At $90 WTI, we can expect US operators to be cutting rigs. That is incredible by the standards of the last decade. What nostalgia one can have for the go-go days of $30 breakevens!

Rig counts

Total oil rig counts: -2 to 494

Horizontal oil rig counts: +3 to 446

The Permian horizontal oil rig count: +2

The Canadian horizontal oil rig count saw progress this week, +3 to 123, but now 5 below this week last year

The US horizontal oil rig count is falling at a pace of -0.75 / week on a 4 wma basis.

This number has been negative for 47 of the last 49 weeks

Frac spreads fell, -2 to 268

DUC inventory, as measured in days of turnover, rose modestly to 13.9 weeks

The Brent Spread (Brent – WTI) remains open, suggesting US shale oil production is exceeding expectations.